Several lads here seem to have a grasp of investments and so on. Do any of you have a regular income outside "earner income"? What kind of category does it fall into, and how did you come into it?

I had a nice image, but brian isn't playing ball today. It's a list of different (very broad) types of income:

1 Earner income : work a job

2 Profit income : buy and sell

3 Interest income: lending money

4 Dividend income: owning stock

5 Rental income: renting out property

6 Capital gains : assets increase in value

7 Royalties: others use your work

Dear diary, I very nearly liquidated my entire portfolio this morning for what turned out to be a -1.24% and AMZN and GOOGL even gained value. The next few weeks will be interesting but I'm glad I didn't succumb to the gloom.

I'm still tempted to go all cash ahead of the new year, even if for no other reason than I'd like to take the chance when the markets choppy to reset my portfolio and avoid having the thought in the back of my mind next week of my portfolio shitting the bed. But then there are a lot of positions where I'll just sell now and buy back in later and a lot of other smaller positions in solid companies that I'd be tidying up for several large ETFs.

>>10001 You trying to time the market there, ladm8?

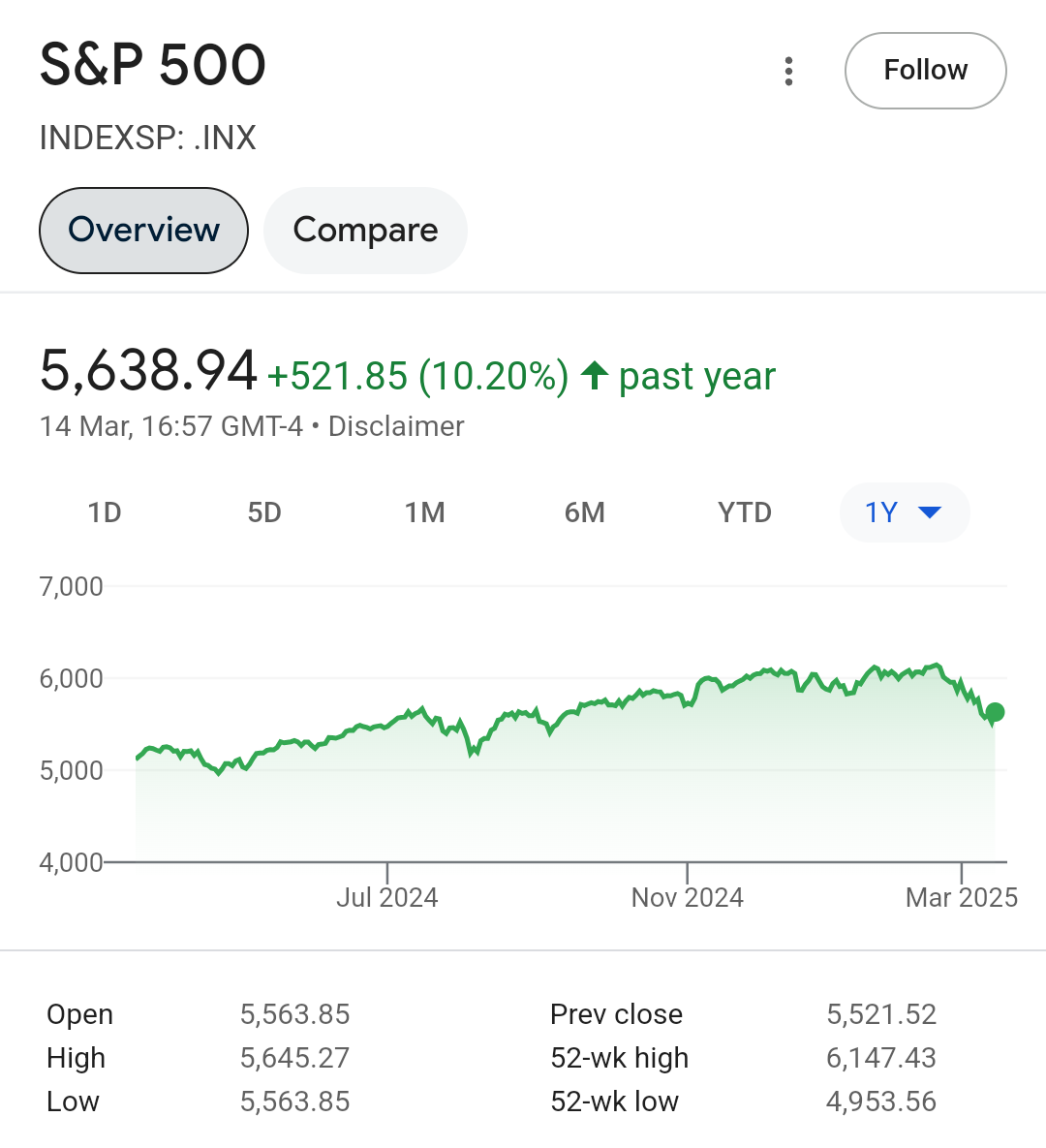

>>10005 >>10006 It's not just the S&P - look at Denmark. We might be heading for a techno-hellscape (unt-unt-unt) but at least we'll have perfect abs and amazing drugs.

>anarchist/communist

Due to the challenges AI poses for the information problem I fear that we'll have to get even more imaginative.

Second Monday in a row of a nasty weekend shock where it looks like trade wars weren't priced-in. I'm actually surprised the indices are only averaging a 1-2% loss.

>where it looks like trade wars weren't priced-in.

The market isn't that short sighted. Trump always said he'd impose tariffs again, and now he has imposed tariffs. I don't think you can really say that it caught the market off guard.

What we're seeing at the moment is profit taking more than anything. Markets were doing well, and they will probably recover quickly. But they were also getting a bit overheated.

I'm tempted to pull out of most of my US investments. The S&P500 tracker especially but I suspect I'm just doing it because I don't like the administration and would put a good chunk into Toronto anyway.

>>10030 You're underestimating the position the US has in the global economy, it's not just that so much of the market is the US investing in the US exclusively but that realistically there's no consumer market like the US.

Gold is now at over £2,200 per ounce. I've inherited a few South African Krugerrand and Australian Kangaroo coins from my parents, and they're now worth almost a combined £17K.

They are family heirlooms, so I'm very generally reluctant to ever sell them. But at that kind of price, I'm thinking maybe it won't hurt to cash in at least one of them. They were all bought in the late 70s by my parents, when an ounce was about £200.

>I wouldn't be so chuffed about 100% over 50 years.

You do mean 1000 percent. In about 48 years.

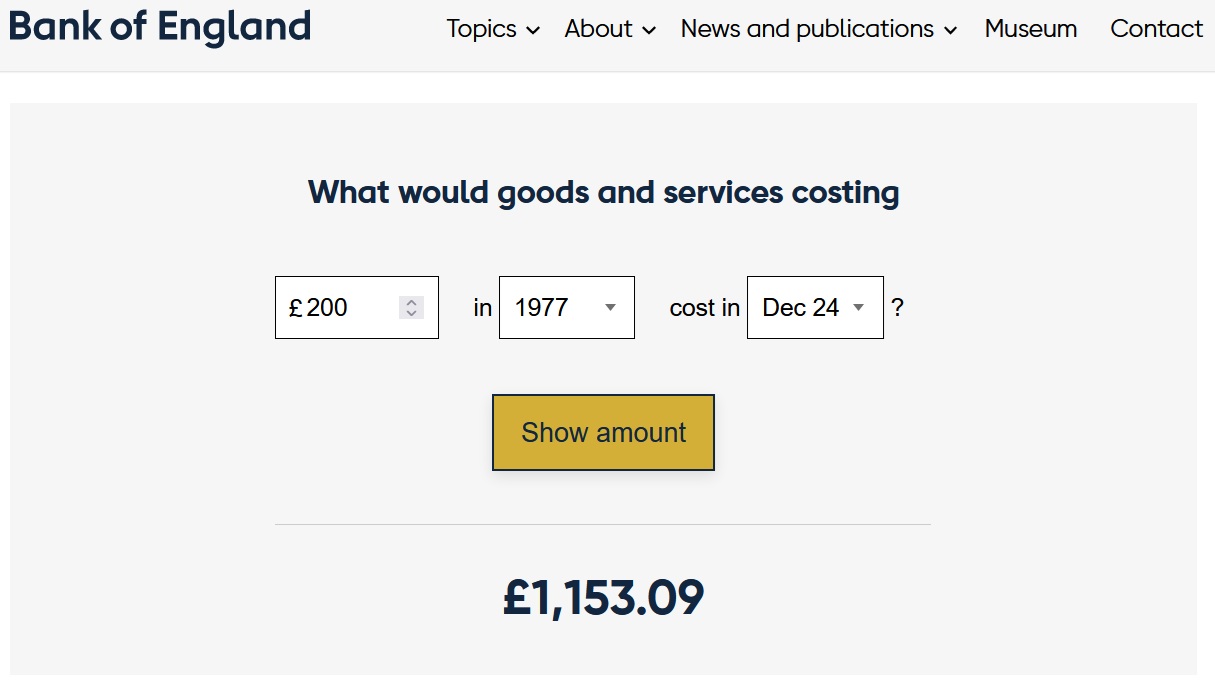

And it's still double the inflation rate. My parents always said that they were about 200 quid an ounce when they bought them. Let's say we take 1977 as the base year, which roughly checks out with the average gold price actually being about 200 quid at that time, according to Google. £200 in 1977 would be £1,153 now according to the BoE inflation calculator. The going rate to sell 1 oz. Krugerrand today, February 17, was about £2,230. Most of the coins I've got are Krugerrand. Which means my parents' investment in those gold coins has appreciated double over inflation. I think that's a decent return. For an asset that was really just left lying in a cupboard for 50 years.

>Several lads here seem to have a grasp of investments

I just looked at my total return over time for my investments (over 6 years, starting the week before the pandemic) by adding together subscriptions and taking away by their current value. And accounting for the 3 times I withdrew money from my account.

LISA Bonus included: 25.54%

LISA Bonus excluded: 43.87%

Now I know why fucking Hargreaves Lansdown refuses to give you a total lifetime return on your account. I would've made a better return by leaving it all in the FTSE100.

I've had some improbable luck trading stock options since last week, and I've made nearly £1,500 just by buying and selling around £5K worth of options each time, and holding them for less than a day. £5K is an amount that I could afford to lose entirely and irretrievably. But I'm still aware that I'm tickling the dragon's tail. And I've been right too many times now, so it's only natural that I'd end up losing if I kept doing it. So I'll stop now.

It's not a sustainable way of earning money. And you will pretend otherwise at your peril. But it's been a thrill.

You are trying to time the market. It's not really a strategy that brings good returns for most retail investors.

It's your decision and your money, but if you don't need the money for the next few weeks or months that you have currently invested, it's probably better to just do nothing.

>>10074 I think it's possible to get lucky once or twice, for example I did very well a few years back by moving a lot of my pension into a gold fund right before things went to shit, it's only really an issue when you become overconfident in your abilities and complacent on the risks of fucking up.

Yes, but that's the point. "Luck" isn't a strategy. You could say that even the best strategy still needs a bit of luck, but if you make your success depend too much on luck, then you've got no strategy at all and you're really just gambling.

I've had incredible strokes of luck where I went in on a stock or an ETF just minutes before they shot up ten percent. Which then well warrants liquidating your position again, because most places, unless you're willing to take on big risk, won't give you ten percent return on investment in a whole year. But it's not something you can bank on. Most of the time, the stock market is kind of pretty shit, and returns are meagre and few and far between. The stock market feeds off investors making wrong decisions. And sometimes, even the right decision proves wrong. You think you're clever by buying a stock that's down 20 percent. And if that slump isn't justified by the fundamentals, then it could well seem like an entirely reasonable decision. But then what do you do when that same stock goes down another 20 or 30 percent in a panic frenzy, and takes years to return to your break-even?

I've been in all these situations over the years, and for me the bottom line is, if you try to time the market, then you're going to lose money nine out of ten times.

And I'm sitting on almost 20 grand worth of gold coins that my parents bought in the late 1970s for a song, in relative terms.

They were all bought in the late 1970s, let's say around 1977, which sounds about right, when an ounce of gold was worth about £250. Which was a fair bit of money, but when you put 250 quid in the BoE inflation calculator, its equivalent today would be £1,447.09. Which means that given the latest sale price for a one-ounce gold coin is around £2,600, gold has outperformed inflation by about 80 percent.

Gold does have bull and bear markets. For one reason or another, there will be a time when gold will go down again. It's going to be impossible to say when it'll go down or even when it'll bottom out. Or what a fair value is for gold.

But with a view to investing long-term, it's probably reasonable to assume that gold will be worth more in 20 years than today, even at current price levels. Because it's a finite resource, and in one way or another there will always be demand for it. At current estimates, all the world's gold reserves, both mined and still in the ground, would probably fit into 3.5 Olympic sized swimming pools. Which really isn't much. If spread all the world's gold evenly across the entire Earth's surface, then that coating would probably only be a few atoms thick.

What do you reckon the US bottom signals will be. I'm fully out of the US but that's very silly by historical norms so I'm trying to draw a mixture of policy shifts, trade war de-escalation* and improved relative valuation to indicate when the market will roughly pick back up. But it feels like everyone is going to have to go off of vibes on this one.

*they won't resolve entirely, trade wars take years with more ups and downs than a Columbian brothel. But they do stabilise.

>Trump says he has 'no intention of firing' Fed boss

>Trump says China tariffs will drop ‘substantially – but it won’t be zero’

>Tesla boss Elon Musk has pledged to "significantly" cut back his role in the US government after the electric car firm reported a huge drop in profit and sales for the start of this year.

He might still spit his dummy out but this could start to look like house training.

> Now try and sell your coins and let us know what the actual profit will be

The nominal profit alone from the 1977 baseline of £250 would be considerable. I'm not sure what you think how selling your gold coins works. The price won't go down if you sell a handful of coins like the ones I have. It's not like selling bitcoin. You'll have no problem selling them to some of the best known precious metal dealers. You'll probably have to deduct a few quid if they aren't mint. Something like £50 per one-ounce coin. But you'll be alright.

I still intend to keep them. As an investment, gold is a no brainer, and has rarely underperfomed inflation in the last 100 years.

The only thing I am getting increasingly uneasy about is that I've got something worth £20,000 in my house that any burglar could just take and steal within seconds. They're well hidden in a spot behind some wood panelling that probably nobody would immediately think of. On the other hand, it's not something that's worth putting in a bank vault, as the fees for it would probably diminish my return on investment. My parents had one for a while, and I think it cost them something like £200 a year. Just putting up with the slight bit of unease of having them in my home is probably the better deal.

>>10082 Was that supposed to be a joke about Bitcoin? Staying away and doubting its future is absolutely fine, but I don't quite understand the need to tell obvious lies.

>>10080 >Trump says China tariffs will drop ‘substantially – but it won’t be zero’

It turns out that this policy shift was provided an hour before it got to the press at a private event for hedge fund managers. Nobody could work out why the market was behaving the way it was until the news broke to the plebs. I know that's entirely expected but for fucks sake.

>>10082 They're not going to give you the face value is my point. You can find plenty of gold hoarders who end up finding out their treasure is worth a lot less than they think when they try to find a buyer.

>They're not going to give you the face value is my point. You can find plenty of gold hoarders who end up finding out their treasure is worth a lot less than they think when they try to find a buyer.

What do you honestly think they're going to give you, and how it works? The value of 999 gold is determined daily on the gold market. Gold coins are commonly 999 fine gold. Which means you can pretty directly deduce from that the sale value of your gold coin.

Most gold coins don't have particular collector's value, unless you have some actually rare ones. Especially series like Krugerrand, Maple Leaf or Australian Nugget, which is what I have, were produced in high volume. What usually matters more is condition. A mint condition gold coin that's never been taken out of its case will sell very close to the daily gold market fixing price, as most gold dealers will sell them on directly to other customers, of course while taking a small cut from you. You could try to sell your coins privately, but most gold buyers aren't comfortable taking gold coins from a non-reputable source. When you buy gold coins through a well known gold dealer, that dealer will have tested the coins, which is usually done through infrared laser spectometry which can tell you at a glance and non-destructively if a coin is real 999 gold, and they will then certify the authenticity to a buyer.

Non-mint coins, which means anything from coins that have been taken out of their case or never had one to ones that have a few dents and scratches usually lead to a deduction, which is currently some £50 per ounce. They end up being melted down, because not many people will buy scratched gold coins. So what you get paid for them is the melt value. Which ends up being about £100 less than the actual daily price at current price levels, but arguably still quite close to it.

I'm not sure where you get the information about "gold hoarders". It can really only happen when somebody doesn't know what purity their gold is. Most jewellery isn't 999 gold, because it's too soft and would scratch very easily, so you usually have 333 or 666 alloys. Especially the 666 will still look very much like pure fine gold, and that is also true to the untrained eye with 333, but it's going to be significantly less valuable than the same weight in 999. I guess that's where most of the disappointment usually comes from.

>They're not going to give you the face value is my point

The term you're looking for is "spot price", which is the instantaneous price of pure gold on international markets. A good dealer will give you about 96% of spot price for coins, or about 94% of spot price for scrap. That's a fair margin in a competitive market. You can sell for around or slightly above spot price if you're selling privately, but obviously that carries a fair amount of risk.

You'll get much less than that if you take it in to your local pawnbroker or send it off to cash4gold, but that's the nature of their business. Their customers aren't tracking the markets and can't really compute the sheer insanity of the gold market over the past 20-ish years; they're just delighted to sell their old jewellery for vastly more than they paid for it.

>>10086 No it's a little joke you see, because they're coins! We like to have our fun here.

My point is you get shafted when you do go to sell even by legitimate buyers which is partly why gold ETFs have taken off. Yes you will get a worse deal on the high-street, partly because they charge a premium for (absolutely not) dealing in stolen goods and desperate buyers.

Markets have recovered a lot of ground, at least for my non-US stuff. All feels a bit too bullish to me and I expect some more crashiness later once tariffs and taxes (thanks Rachel) start hitting earnings.

>>10090 This is one of the problems I've got at the minute - you have a situation where sensible moves feels overvalued while we're nowhere near the bottom on tech. Interest rates are falling but equally I see us getting a price shock or two either when the US/Israel turns attention to Iran (Trumps is already throwing out demands) or otherwise the US spits its dummy out because it's still not been burnt hard enough yet.

I'm tempted to gamble on logistics like Prologis where a short-term play might work but I'll probably just park some money in Japan.

Markets are always volatile, temperamental and unpredictable. Right now the moves in both directions may seem big, but it's worth remembering that in the months before Trump's harebrained tariffs hit, there was very low volatility. And prolonged phases of low volatility do tend to resolve into ensuing phases of sheer abject panic and whiplash moves.

Yet again, all the Chicken Licken "the sky is falling!" and "but... but... it's different this time!" histrionics that you fannies love to get caught up in has proven to be a load of bollocks.

>>10114 Every time there's heightened market volatility posters on here completely lose their heads and start catastrophising. Every time it happens the markets eventually settle, but they'll still shit the bed the next time it happens.

This is why I'd never take investment advice from you lot. You're massive fannies who can't hold their nerve.

>>10115 I hold my nerve so I don’t post. I just have a load of money somewhere that I never touch it, and it goes up a bit. If you get your impressions only from the people who post in this thread, then of course you will be getting a selection bias of only people who want to say things.

And I would argue that the reason Trump reversed all his tariffs after saying he would never do that was insider trading because the sky did in fact fall.

>>10116 >If you get your impressions only from the people who post in this thread, then of course you will be getting a selection bias of only people who want to say things.

That's like saying .gs must have good taste in women because the majority are being silent when there's posts about shagging Scarlett Moffatt or Ladbaby's wife. Anyone who thinks this is a site full of chubby chasers has fallen foul of selection bias.

While we're on the topic, I assume spread betting isn't a good way to invest long-term, as my profits are probably being eaten away by overnight fees.

Despite being a spread better (gambler) I am one of those plebs who is suspicious of stock markets, even if, as proponents argue, it offers 'objectively' better returns. I wish it was as easy to buy gilts as it seems to be to buy T-bills in the US with Treasury Direct - I'd be happy to just clip coupons and sleep easy.

I'm also bullish on gold, because of the state of the world, more than any belief in the fundamental value of shiny rocks, but I cba to buy gold directly. Are gold ETFs/ETCs worth it?

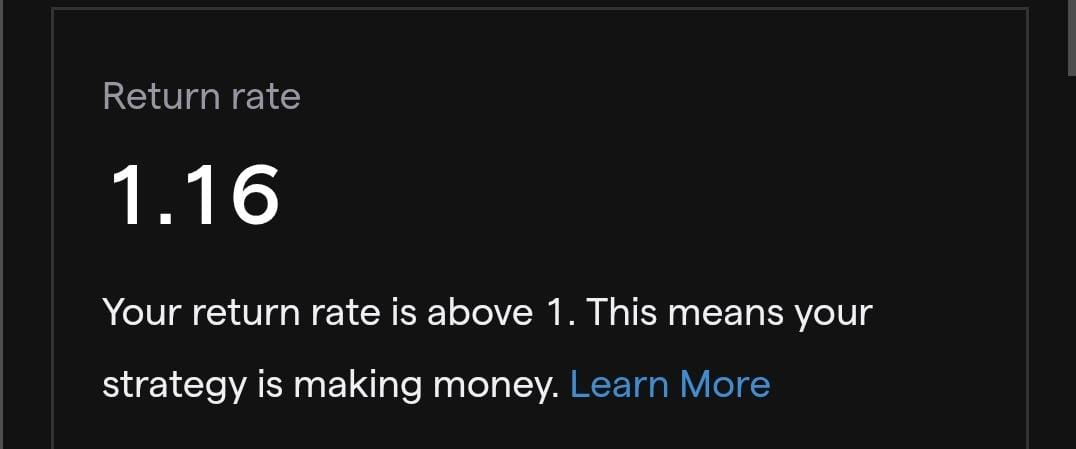

>>10124 Over 70% of DIY investors lose money so if you want to look at it that way it's not bad. But it depends on time period, 1.16% across the portfolio is a nice day but if it's a year then you're money is just inflating away.

I got burned once with Tesla stock, lost about £3,000 in two months in early 2022 when the stock did something it had never quite done before by going almost 40 percent straight down. Granted, the stock has made repeated comebacks since then, but all in all, I don't think I'll ever get in again. And with everybody's favourite heavy drug user CEO at the helm, it will probably always be a seesaw.

What people get wrong about big volatility is that they only see the rip-your-face-off spikes of a stock in strong bull markets. But the true meaning of volatility is the likelihood that a stock will behave differently than expected by many investors, and sometimes violently so. Volatility therefore always increases risk same as it increases possible profits, but for the typical retail investor who usually turns a loss either way, it will more often than not only make that loss even bigger.

The FRDM ETF is exactly what my portfolio needs but I still can't invest in it while it's making more and more growth with a thesis on emerging markets that just makes sense. They're still talking about seed funding for a European equivalent which means we might be years off being able to buy into the idea.

It feels like investing even in the UK is still treated as a unserious business and that if you want to invest you should just move to the US. The ETF market in particular takes the absolute piss when it comes to giving people real choice and where you do find more niche options the fees are extortionate.