>Let’s call her Laura. In September, Laura was out in Leeds City Centre, buying some bits, when her card was declined. Funny, she thought. She definitely wasn’t in the red. But these things happen, so she left the shop, tinting crimson, and dashed towards the nearest cashpoint. But her card wouldn’t work at the cashpoint either. She tried another one. With the same result. Laura opened the banking app on her phone. It said only ‘error’, then automatically closed. She finally abandoned her shopping and went into the nearest branch of Santander. There, the counter assistant seemed just as mystified. After about an hour of waiting, though, Laura was called through into the manager’s office.

>“I’m going to read a statement out for you,” the manager said. “But I’m not going to be able to answer any of your questions after that. We have locked your bank account. We can’t give you any more information. We might be in touch in future with more information. But we don’t know when that might be.”

>Could she have her money? No. But how was she supposed to get home? After all, she lived eight miles outside of Leeds, and now she had no bus fare. Apparently, this was not the bank’s business. This low-rent version of The Trial went on for another three weeks. Frequently, Laura would phone up Santander customer services. She’d be put on hold for ages. Then the phone would just go dead. She wrote to Santander to complain. They wrote back: they weren’t interested in her complaint and wouldn’t be taking it any further. Meanwhile, her rent, standing orders and Direct Debits stacked up, the late fees and penalties mushroomed around them, as life tumbled towards chaos.

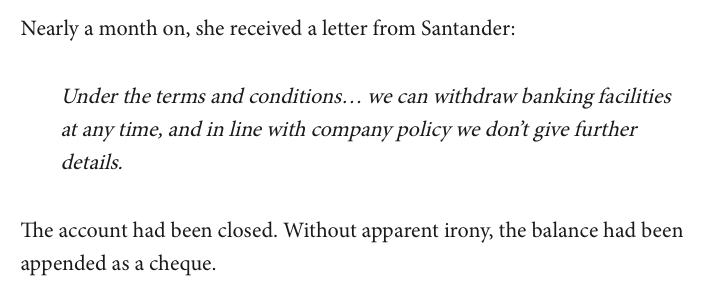

>Nearly a month on, she received a letter from Santander: Under the terms and conditions… we can withdraw banking facilities at any time, and in line with company policy we don’t give further details.

>The account had been closed. Without apparent irony, the balance had been appended as a cheque.

Reading that was quite unsettling. What is going to be the impact of unpersoning in a society that is increasingly cashless and driven by online transactions?

Gordon Brown tried to instate a right to a bank account but it was shot down by the banks themselves. I think it underlies how our society is now underpinned by effective public utilities that remain subject to a belief in a right to refuse service and which then effectively become tools of social control outside of the remit of even the state - an AnCap dream maybe but more like a nightmare that borders on the social credit system of China.

It is a very scary prospect and the type of thing that can creep up slowly. One of the reasons I have obly used cash during the whole debacle this year.

>>5062 ‘Laura’ could be any of us. But she is also Laura Towler, one of the founders of Patriotic Alternative. Towler is a sort of next-gen BNP type, a net-savvy white identitarian who campaigns against mass-migration, and occasionally winks to her Telegram followers about ‘you know who’ (they know alright: The Jews). It would seem that Towler had been expelled from Santander for her views. But in line with the bank’s conditions, this has not been made clear.

I am guessing that she became what is known as a Politically Exposed Person. I am also guessing that she was getting donations from people, for her nascent political party. At that point, for any bank, you're going on a list.

I don't want so suggest its fair, but at that point your bank is going to red-flag your account and it will go for manual review. If that person then finds you're then espousing controversial / dicey opinions, plus taking donations (I am still guessing at that bit) then they totally have the right to not want to be associated with you and close the account.

So my point is, this doesn't just happen to random people.

>>5066 We don't have any information about how those people were operating their accounts. Were they getting regular payments or making payments to risky places? Are they getting regular, non-standard cash payments of a risky size? Are they associated through family to people who are PEPs or fraudsters?

Again, I'm not making value judgements about those people or activities (although in Laura Towlers case I probably would) - just trying to describe how the system(s) work. The only cases I have seen where this happens by accident is if you share the same name as a fraudster or PEP.

>>5068 They did though - probably after checking all the payments she was getting and making sure a Suspicious Activity Report was correctly filed with law enforcement authorities.

I would make an assumption that this is linked to the USA Patriot act, which compels banks and payment providers operating in the USA to police their customers for suspicious activity, on the grounds of "preventing terrorism".

Otherlads have suggested that she's probably been getting donations linked to her quasi-political party, and its most likely that the banks are looking for any sort of activity like that regardless of which country the customer is in to make sure their records are squeaky clean.

>>5070 No, it is UK-based - the Financial Conduct Authority mandates all of this.

Your second part is right though, banks in the UK are extremely regulated by the FCA, the PRA and to be honest, don't want the grief of dealing with dodgy customers who might be fraudsters, terrorists or politically exposed persons. Law enforcement authorities and successive governments of all stripes have put these regulations in place because they often can't catch people in the act of doing a crime, or deter those crimes, but they can easily regulate the banks into oblivion to "follow the money" and do it for them.

I think the lesson here is "if you're going to run a neo-Nazi fundraiser using your personal bank account, you should probably keep some cash on hand for emergencies".

>>5072 Santander are really keen on combining accounts and cross-funding if they feel like it.

They tied together two of my company accounts and a personal one, and would casually take money from whichever account contained it. For my convenience, and because fuck you.

So, keep your nazi contributions in a completely different bank, and hope they don't buy each other.

>>5073 >They tied together two of my company accounts and a personal one

They're totally allowed to do that, unless those company accounts are Limited Company accounts. You just didn't read the T&Cs. In the context of an individual person, account means nothing. A limited company is like a person in its own right, separate from you.

Don't keep your nazi contributions in any bank account, or any financial institution or electronic money company that talks to CIFAS (protip: everyone does). That includes PayPal. I bet in this Laura Towler case it was PayPal donations that did her.

>>5076 They are indeed limited companies. They apologised. I didn't ask for the accounts to be linked in any way - the second company's account details suddenly became accessed from the first company's login page, along with my personal account. And then they did the cross-payment thing.

The same two people had login rights for both accounts, but combining companies did seem like a dodgy optimisation.

>>5081 If that's the case, then you should complain to the Financial Ombudsman - again, banks don't want the grief of dealing with regulators, so a complaint to them will almost always find in your favour if you have an actual case. It takes about 90 days, but if they've genuinely fucked up and cost you money, you will get it back.

>Bank bosses have made a commitment to free speech, according to the government, in the wake of the Nigel Farage de-banking row that claimed the scalp of NatWest chief executive Dame Alison Rose. Her four-year tenure as chief executive ended in ignominy last night following her admission that she had discussed Mr Farage's bank details with a BBC journalist, suggesting too that his account at the bank's Coutts division had been closed only for commercial, rather than any political, reasons.

>Treasury minister Andrew Griffith met 19 bank bosses for a summit on Wednesday to discuss concerns other figures, not just Mr Farage, were being denied access to banking due to their politics or perceived beliefs. Mr Griffith said afterwards: "It's not the job of banks to tell us what to think, or what political party we should support. "The government's been extremely clear on this, in a democracy that relies upon freedom of expression... that is not a legitimate thing for a bank to remove someone's access to a bank account."

>A readout of the meeting's conclusions suggested the industry had agreed to work with government and regulators on the implementation of new rules aimed at strengthening protections on account terminations or access to accounts. Attendees from the sector acknowledged that recent events had impacted upon public trust for the whole sector and expressed their clear commitment to government policy on account closure and to act quickly to restore confidence," the document said.

>The former UKIP leader also said he hadn't been able to open another bank account and claimed he has been turned down by 10 banks. Mr Farage also claimed he has been "approached by literally thousands of people all over this country that have been unfairly closed down by NatWest".

>The story first came to light when the BBC inaccurately reported Mr Farage's account was closed as he did not meet Coutts's financial thresholds. Documents obtained by Mr Farage subsequently showed his political beliefs and connections formed part of the rationale. Mr Farage told Sky News he has written to Peter Flavell, head of NatWest's Coutts unit, "three times" since his account was closed and had not even had the "courtesy of an acknowledgement".

https://news.sky.com/story/natwest-boss-steps-down-with-immediate-effect-over-nigel-farage-bank-account-leak-12927506

Looks like they forgot the first rule of plutocracy that you don't unperson populist celebrities.

When he asked them to apologise the BBC should have claimed he fell below the wealth limit because he'd been paying "tuition fees" to eighteen year old Romanian girls.

Ugh, don't you just hate it when international megacorporations give the little fascist on the street a voice by engaging in dystopian unpersoning practices and then lie about it in secret to BBC News.

The full story is a bit more boring and complicated than either side is making out.

Farage fell below the wealth limit and Coutts in part decided to close his account because of his politics.

Coutts is a very exclusive private bank that offers an exceptionally high level of service to very wealthy people. Farage's political exposure made him an unusually expensive customer to serve, even by their standards. When he paid off his mortgage, they made the decision to close his account because they weren't making enough money from him to justify the effort. It wasn't wokery, it was just a cynical financial decision from a cynical financial institution. They were perfectly happy for him to have a NatWest account, they just weren't willing to continue providing a super-deluxe banking service at a loss.

This whole story has blown up because of Farage's extraordinary political alchemy - he manages to portray himself as an everyman railing against the elite, while also getting massively bumsore about having to have a normal bank account like the proles.

People regularly pop up on reddit complaining they have lost access to their bank and the bank won't tell them why.

The usual explanation is that some bank AI (mandated by government KYC regulations) has decided they might be doing some fraud. In such situations they bank is not allowed to say why they have frozen the account.