>Mr Johnson also channeled the spirit of Thatcher's 1980s revolution by pledging to save the dream of home ownership for a new generation, with the government underwriting 95 per cent mortgages for around two million first-time buyers.

>The government has yet to give details, but it seems some of the 'stress test' rules imposed on banks after the 2008 financial crisis could be relaxed to facilitate long-term fixed rate mortgages at 95 per cent of a property's value. The government could instead accept some of the risk through a guarantee scheme - although this would leave the taxpayer on the hook for potentially huge sums.

>>96230 Specifically: the energy producers are making all time record profits. Domestic suppliers are facing the same squeeze as the rest of us. I'm sure someone will say something about corporate law preventing those groups from using their Lolo Ferrari level inflated profits from their generation arms to cross-subsidise their domestic supply arms, but fuck it - nationalise the production. Some people will complain about the government undercutting prices to sell oil and gas cheaply to UK suppliers but what is a government even for if not looking after its own people?

Since this used to be the housing thread, let's take a brief break from Boris to become truly angry:

https://www.bbc.co.uk/news/business-62075834 >House prices hit a fresh record in June, according to Halifax, despite expectations the rising cost of living in the UK would dampen demand.

>The mortgage lender said the average house price reached £294,845 in June after rising by 1.8% - the steepest monthly increase since 2007.

>Halifax said that the housing market had, so far, been largely insulated from the rising cost of living.

>"This is partly because, right now, the rise in the cost of living is being felt most by people on lower incomes, who are typically less active in buying and selling houses.

>In contrast, higher earners are likely to be able to use extra funds saved during the pandemic," said Halifax managing director Russell Galley.

>House prices rose by 13% in the year to June, which Halifax said was the highest rate since late 2004.

The article goes on to say house prices won't keep going up forever, but as it admits, that's already been predicted once and they were wrong then. And whoever our new Prime Minister will be, it's almost guaranteed to be someone who wants house prices to keep going up, because that's how these fuckers win elections.

Well, I mean, that's kind of the point, it's semantic argument if it's the producers or suppliers. If it's the suppliers struggling that means we have to pay more, then it just demonstrates what pointless parasite middlemen they are, like estate agents and record labels.

Seize the lot at the source I say. Energy should be non-profit. Instead of a high bill for everyone, just whack a tariff on households using too much.

>>96232 >>96233 Housing and energy are experiencing the same fundamental problem of a lack of supply that is driving prices and there's no immediate solution in either category that doesn't involve demand destruction.

If I'd known we were doing the Pacific Campaign I'd have brought a flamethrower down to London, rather than waiting for him and carrier to take cyanide.

Apparently there are to be "no new policies" either, until a new useless lump takes over. I'm sure Braverman or Shapps will get on top of energy prices in the four weeks they'll have to do so.

>>96234 >>96235 Did the monarchy rescind it's claims on France or did both families quietly agree to put it to one side? Perhaps it's time France had it's first female president?

I struggled to type that even in jest, such is my distaste for the royal family.

>>96238 You can't blame me for what happened in 1800. If I'd been in charge we'd have been best mates with Bonaparte and conquered the world together. Today, we'll simply have to get more creative. See if you can dig up and anglophone discrimination going on in France, that old bollocks is all the rage nowadays.

Nah, bugger that, Napoleon's regime was the most despicable thing of all- Liberal.

What we should have done is thrown our lot in with the Queen's cuz Wilhelm II in the first world war. Leet them have Europe on the land, while we rule the waves. Never need to let America rise up and utterly shag everything for the rest of us.

I've made this point before in relation to many industries, but it bears repeating - if the energy industry was run on a not-for-profit basis, most people would hardly notice the difference.

In the last financial year, BP made net profits of $8.5 billion, but they made that on revenues of $164 billion. In the best case scenario, completely removing their profits would lower the price of a litre of petrol by 10p. You could perfectly reasonably argue that it would still be worth doing, but a 5% discount on fuel is hardly a glorious socialist utopia.

The other part of the equation is that those profits aren't going to some imagined greedy fat cats, they're mostly going to ordinary people. If you pay into a pension, you're almost certainly a shareholder in several energy companies. If we just confiscate the energy industry, we're confiscating it from you, or people like you.

It seems to me that the main argument power should have always been nationalised is about efficiency and ecological responsibility, not zero-sum affordability.

The situation we have now means energy countries are committed to running the wells completely dry on fossil fuels before they even think about making serious efforts to commit to renewables, because to do otherwise just leaves money on the table, from their perspective, wasted. If energy companies had been run as a purely utilitarian service funded by the taxpayer, we'd have had everything running on nuclear, wind and solar decades ago, because the incentive would have been to just go for whatever provides the largest and most stable long term supply, rather than maximising the profit of existing investment in fossil fuels.

>>96241 >The other part of the equation is that those profits aren't going to some imagined greedy fat cats, they're mostly going to ordinary people. If you pay into a pension, you're almost certainly a shareholder in several energy companies. If we just confiscate the energy industry, we're confiscating it from you, or people like you.

There's a part of me that has very strong opinions about this from an accounting identities perspective, despite not being an accountant.

What I mean is: If you have all the profits that flow to shareholders flow to the state, then have the state give the money to pensioners I'm a happy bunny - but if have them flow to pension funds as we do now, and then to pensioners, and it's clear to me that our economic system is a complete sham and that the complete collapse of industrial society would be philosophically preferable to its continuation because at least it would be "honest".

I'm not defending the status quo, just describing it.

The left recognise that a lot of right-wing arguments about things like immigration are based on assumptions and falsehoods, but they don't recognise that a lot of their economic beliefs are based on vague intuitions rather than actual fact.

It's an article of faith in left-wing circles that "the rich" have got so much money that we could fix everything if we just redistributed it fairly, but that belief just doesn't stack up.

Companies make "huge profits" relative to an individual's income, but their profit margins aren't actually that large and eliminating profit wouldn't make anyone significantly better off. Billionaires are very wealthy, but there are only about 2,000 billionaires in a world with seven billion people. Setting aside the fact that most of their wealth is in the form of shares in companies rather than cash in the bank, redistributing that wealth wouldn't be life-changing for the vast majority of people in developed countries and would come with a lot of very complicated and dangerous economic side-effects.

The world is unfair, but nearly everyone in Britain is a beneficiary of that unfairness. Someone on exactly the average salary in Britain is in the top 2% of earners globally. Someone getting the minimum amount of state benefits is still comfortably in the top half. Anyone calling for the downfall of capitalism and radical redistribution should be careful what they wish for.

Do you have this saved to your clipboard or what? Spare us lad, nobody's in the mood to hear about how the rich aren't actually that rich, you can't go taxing them a bit more to redistribute wealth more evenly because the poor dears are only barely making a profit! Silly socialists!

No, the thing is you can come to the conclusion our economic system is totally fucked even as a capitalist. You don't have to be a committed Marxist to realise that our levels of economic inequality and the rampant state of speculation, the property bubble, and personal debt combined with policies like quantative easing are propelling us toward a crash on the scale of 1929. The conditions of our current economy look exactly like they did 100 years ago, just with more smartphones. You don't have to be the kind of person who wants to hang all the bankers in the streets to understand that we've let the cart run away with the horse and that action needs to be taken to stop the whole house of cards collapsing.

The Owen Jones crew might overestimate how wealthy the rich are, but there's no way of avoiding the fact that whichever way you slice it, the rich are too rich, the neoliberal belief in trickle down economics is beyond a dead horse at this point. You don't have to be a socialist, you just have to be aware of history. They teach this stuff to kids in GCSE history but our politicians and financial elite seem to be none the wiser.

What you fail to account for is that a lot of socialists take a very keen interest in economics, because understanding the system is vital in order to form a rational criticism of it.

>Anyone calling for the downfall of capitalism and radical redistribution should be careful what they wish for.

Which is probably why outside of niche rudgwicksteamshow.co.uk communities and university clubs, you'll find very scarce few people seriously and earnestly wishing for that. What you will find people wishing for is things like a more progressive taxation system, a tightening of regulation on certain markets and financial systems, rules capping how much bosses can be paid compared to their workers so that everyone sees a fairer share of the fruits of their labour, things like that.

It's fairly obvious to see that every attempt at a command economy has inevitably collapsed, and the only one that succeeded converted back to a version of capitalism. It's a matter of what works for what, and the full on Society style of socialism unarguably works very well at one thing- Industrialising an economy that was otherwise stuck in the feudal age. What it doesn't do so well at is providing continued growth past the industrialisation stage. This is why we see China continuing to prosper instead of stagnating and collapsing like the USSR did- They used the full on Soviet style system to kick off their industrial revolution, which is what it's good at, and then went back to a more liberal economy, and currently they're benefiting from what that's good at.

What we need to solve in the West is the next stage. What needs to take over from liberal free market capitalism now that we've reached the end of it's usefulness? We're clearly seeing we've got to the point that this economic system is struggling to deliver any more. The apex of the curve has been reached. The point of diminishing returns. The point at which the inherent flaws start to grind against and drag down the benefits.

Where China has an advantage over us is that they have a government that can and probably will make that change when the time comes for them. They'll hit the button and advance to the next age, build their wonder before us because we've been sitting about waiting for Elon Musk and the Free Markets (that'd be a good band name) to do it for us, and win the game.

>It's fairly obvious to see that every attempt at a command economy has inevitably collapsed, and the only one that succeeded converted back to a version of capitalism.

That's first-semester economics stuff really.

What you're also made aware of in first-semester economics is that capitalism may be superior to a centralised planned economy, but it is far from perfect. What capitalism has going for it is that it has a tendency to use resources relatively efficiently, because individuals who own those resources have a desire to if not maximise their profits, then at least receive whatever they feel is an adequate return. Socialist and communist governments have proved incapable of steering and controlling the efficient use and application of a country's economic resources in a way that capitalism is mostly able to. I say mostly, because just look at market bubbles in capitalist systems. Market bubbles mean that a market becomes crowded, and will see decreasing returns in the near-term or could even crash. Like, for example, tech stocks in the last six months. And yet, resources are still allocated into those bubbles in the belief that there will be continuing returns and that you're smart enough to bail out before the crash comes.

Another interesting aspect to look at when comparing socialism and capitalism is wealth and distribution. Wealth distribution is one of the core values of socialism, to the point that at least in theory, it dreams of a world where wealth is entirely equally distributed and where nobody has more or less than their neighbour. The problem is that because of socialism's inherent inefficiencies, a country's wealth may well be distributed more equally than in a capitalist system, but overall wealth and standards of living in socialist countries tend to be far lower than in capitalism. On the other hand, it goes without saying that capitalism has a tendency to concentrate wealth in the hands of the few. Which is why unbridled capitalism, despite a usually more efficient use of resources, generally doesn't lead to a great increase of social and overall wealth. And that's why few countries today practice capitalism without a whole host of safeguards and limits on wealth concentration.

The mortgage affordability test has been scrapped. Now, if you have a whopping deposit and whopping income and can buy a house, but you keep getting turned down for a mortgage because you wouldn't be able to afford the repayments if interest rates went up and your repayments were suddenly much higher, you will finally be able to get a mortgage anyway.

Why on Earth would they introduce this now, at a time when interest rates really are going to go up and the general cost of living really is skyrocketing? A lot of these people are going to potentially find themselves a lot less worth lending to. A lot less prime. Subprime, if you will. Where have I heard that word before?

>>96567 For renters trying to buy being told they might not be able to afford their repayments if interest rates went up, what do the people telling them that think is going to happen to their rent?

>>96567 It seems like people are getting a bit myopic over mortgage interest rates. They were extremely low in 2020 and 2021 but now they've drifted back to the ballpark of where they were roughly between 2015 and 2019.

Yeah, it's annoying if you've missed out on a five year fix at about 1.8% but having to fix at 3.5% like people would have done in 2018 really isn't the end of the world. It's not worth losing your head over something reverting to the mean just because you've decided to use interest rates being temporarily depressed by a global pandemic as your baseline rather than as a brief anomaly.

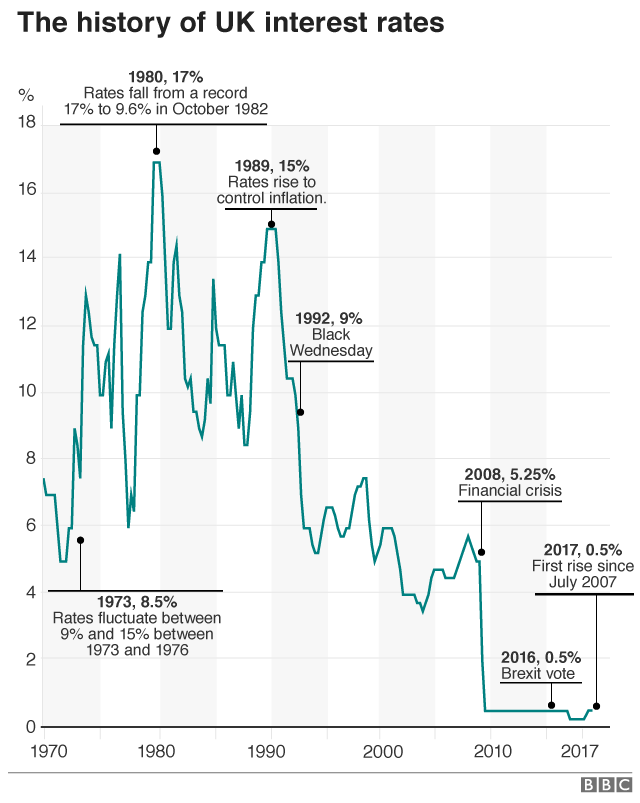

Inflation is at 10%. Liz Truss is proposing an economic package that could push the base rate up to 7%. It would be an extremely big deal if those people discover that at the end of their fixed rate deal their mortgage payment will double.

Why does nobody have a mad plan like capping interest rates for current mortgages while leaving new entrants to the market?

I can think of a lot of reasons that go along the lines of "Oh, it'd distort the market", and a few on the lines of "oh it's unfair", but it's not like the housing market isn't already a deeply unfair circus, and unlike building new council houses or help to b[id up house prices even more] this stupid idea wouldn't even cost the government any money beyond the printer paper the legislation would go on.

I suppose you might lose the votes of people who want to buy their own home, but they're probably already unsympathetic to the Tories compared to people who think they own the bank's home and would like to maintain that illusion.

I read recently that something like half of all sales are falling through at the moment, with that figure rising to two thirds for first time buyers. I think the obvious answer here is that they're desperately trying whatever they can to stave off a property crash that's beginning to look inevitable- Like any bubble, it's got to burst eventually when nobody can afford to buy in anymore, and this one has got well past that point.

Question is, does that mean now is the last chance to buy and save yourself from a lifetime of renting? Or is it the worst possible thing you could do, wasting a shit ton of money and then getting fucked in the collapse? Or, frankly, both?

Either way it feels like times have genuinely changed. The prosperity we took for granted for so long is looking like it might very well be a thing of the past.

Loads of people took out fixed-rate mortgages the last few years, so the interest rate hike isn't hitting them immediately. It'll only come to bite them when their fixed term runs out and they're suddenly faced with double or triple the payments.

It may sound elitist, but the last few years, we were at a point again where people were financing homes who weren't normally in a financial position to buy property in the first place, and could only do so because interest rates were low and mortgages were piss easy to come by because banks didn't know what else to do with their money in times of zero interest.

Not in similar numbers as during the subprime crisis, but there was certainly a trend towards that. It shouldn't surprise anyone that people who got a mortgage by the skin of their teeth are now the first ones to get washed out as lending market conditions become less favourable.

I'm just saying that whether or not you can afford to buy a mortgaged property depends on your ability to keep paying off your mortgage during times when interest rates rise.

>>96576 >It'll only come to bite them when their fixed term runs out and they're suddenly faced with double or triple the payments.

A 30 year mortgage for £200,000 at 2.5% would come to £790 per month. If that goes up to 5% then that'd go up to £1,074 per month, so up by about 35% but that's completely ignoring the fact that you should be in a lower LTV band and have access to better rates.

>we were at a point again where people were financing homes who weren't normally in a financial position to buy property in the first place

Were we though? Who were these people? Because I don't know any of them. I only know people for whom getting a mortgage has always been perpetually just out of reach, and keeps on staying that way as prices rise directly in line with their ability to save for a deposit.

None of the people I know who couldn't really afford a mortgage have ever been given a mortgage, because they couldn't afford one. The banks have never exactly walked around handing out mortgages like lollipops.

Now, I know a fair few people who probably got a bigger mortgage than they should. And I know a couple of people who have one or two more mortgages than they probably should have (interest only at that.) Is that perhaps more what you mean?

>>96575 >Question is, does that mean now is the last chance to buy and save yourself from a lifetime of renting? Or is it the worst possible thing you could do, wasting a shit ton of money and then getting fucked in the collapse? Or, frankly, both?

My offer has been accepted and the mortgage is set up, but it's all gone a bit quiet. So I really am right on the precipice. If the sellers pull out, I'll be frustrated but hopefully more houses will become available and they might be nicer than the grim shithole I've bought. If they don't pull out and the house is mine, house prices never go down so I should be all right. And after the interest rate panic that's currently happening, they will drop down again to rock-bottom to stimulate the economy once my fixed-rate mortgage expires. Hopefully, hopefully, I'm the king of the world and not actually fucked beyond belief.

>>96576 It shouldn't surprise anyone, but I'm not really approaching this from a position of sympathy for people on mortgages. It's more a question of buying votes - if people are on mortgages they can't afford, why not bail them out, or at least delay the inevitable until it's Labour's problem? If people have started voting Tory because their not-so-viable mortgage makes them feel richer, why not keep them on side? Their inability to pay might only be a problem at the end of a fixed term, but you'd think there'd be a plan sitting there for when that happens.

I assume there's a flip side where the banks won't like it and they might not give you campaign funds and directorships if you annoy them too much, but equally I assume they'd rather be stuck breaking even or taking a slight loss to getting stuck with devalued houses in a buyer's market.

Right so what about if, right. What if, we staged a sort of mass property sale sabotage?

Like, what if we all put in offers on houses, and pretend like we're going to go through with buying them, but then just fuck them about for a while and eventually drop out? You could do it with multiple houses at once as long as it was different agencies.

I'm not sure whether it would achieve anything positive but it would at least disrupt the flow of sales right? So it should do something, at least.

>>96669 Unless you're pretending to be a Russian oligarch or an Arab oil magnate, they're going to insist on the AML and KYC stuff, which means that you're going to have to give your real details to all those agencies in order to make those offers, as well as a proposal on how you're planning to fund the purchase.

If you do decide to pretend to have money to launder, you won't be affecting anyone other than the super-wealthy with expensive properties to sell, because no agency is going to let you buy on the DL unless the seller is also in on the scam. So while you might be inconveniencing the sort of agent and the sort of seller that's willing to engage in money laundering, you're not going to particularly disrupt the general flow of sales.

You'd only need a mortgage in principle and a valid ID to get past most of those initial checks. People who are already home-owners can even join in in solidarity by pretending they're selling their house. Then once the seller has accepted the offer, you can take a few weeks to say you're instructing a solicitor and such, but obviously never do, then phone them up to say "Oh really sorry, but I'll have to back out, my dog died" or some shit.

So far as I can tell there's nothing illegal there, and it's nothing to do with money laundering. You're a completely legitimate person who, for all they know, is legitimately planning to buy the house, and then just doesn't. Even if you only disrupt them by a couple of weeks before they re-list it at the estate agent, it should cause enough disruption if only a few hundred people do it to seriously clog up the system.

The question is more exactly what effect that's have on the market.

>>96669 >Like, what if we all put in offers on houses, and pretend like we're going to go through with buying them, but then just fuck them about for a while and eventually drop out? You could do it with multiple houses at once as long as it was different agencies.

There's a reason many landlords hate dealing with Asians. They pull shit like this all the time.

Speaking of the property market, what's the best way to fuck with landlords on deposit-only mortgages? Prices are way to high and either supply is too low or the market is moving too fast, and since my landlords have decided that apparently they no longer want me after a decade (probably because they could get around 50% more with current market rents) I'm struggling to find anywhere to live.

(As to the prospect of negotiating with the current landlords, I've already batted back on s.21 claim because the letting agents appeared to backdate the notice.)

>>96671 >You'd only need a mortgage in principle

Don't those require hard searches and recorded applications? That might put a damper on trying to get an actual mortgage, or satisfy any other requirement for good credit.

>>96675 No. This scheme will absolutely get you blacklisted by every estate agent and prevent you from ever buying a house, but a mortgage in principle only requires a soft check and you can even get several at once if you like. It's all automated so you aren't even inconveniencing the banks by applying for them all.

Sorry. It's me (and possibly otherlad's) fault for finally getting on the property ladder. This is just how it always is with me.

It's just like when I was in school, as soon as my year did our GCSEs and left, they built a big new computer lab with loads of top of the line workstations. Or like when I was trying to start a business as a young lad, and as soon as we found a suitable property to use, the council re-zoned that land so our use case would be illegal.

Everything either gets better once I am no longer there, or it goes to shit as soon as I arrive. I could probably end capitalism by becoming a banker.

What does this mean for BTL landlords? Less incentive for renting means more availability of housing for normals? Or will Johnny Foreigner instead buy up houses as a means of parking money in a safe country? Is the English Property Market even a safe place to park money now with Bumder Truss blowing up the economy with her mini budget blunderbuss?

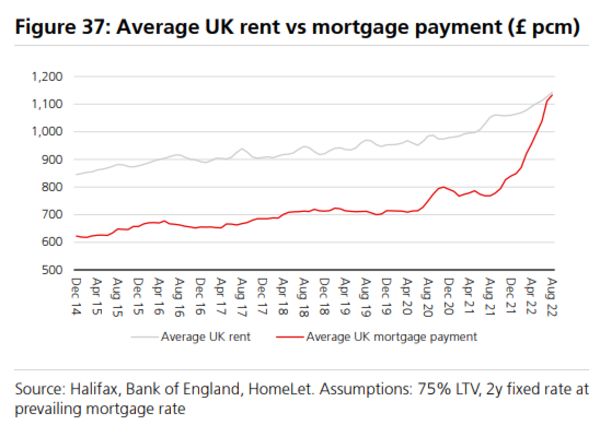

The knock-on effect of a slowing of house sales has been a significant surge in demand in the rental market, alongside a fall in landlord instructions for new lettings.

“Near-term expectations point to a further strong growth in rental prices over the coming three months,” said RICS.

Increasing rental rates will help landlords when they come to remortgage their properties, but as many as 30% of those with buy-to-let loans are likely to fail their renewal test, according to a report by credit rating agency Moody’s on Wednesday.

In order to refinance, buy-to-let mortgage holders have to meet affordability criteria, based on a minimum interest coverage ratio (ICR), that soaring interest rates makes more difficult to meet.

“A 4% increase in interest rates by the end of 2023 would push 30% of buy-to-let loans below their minimum ICR requirement,” said Carmen Brunetti Llavona, analyst at Moody’s Investor Services.