Lads I forgot it's new years eve. What fund should I put 4k on for this year?

I'm considering ASI Latin American Equity to have some exposure to emerging markets but it would make me a slave to US yields. Might instead just put it all on FTSE250 if we're going to have a sharp recovery this year.

It's not new years, it's not even tax new year for a few more minutes. That said, Vanguard is and remains a safe bet. Unless you really want to get into active trading an LS80% S&S ISA is a good bet. I like to gamble a bit, spread attached.

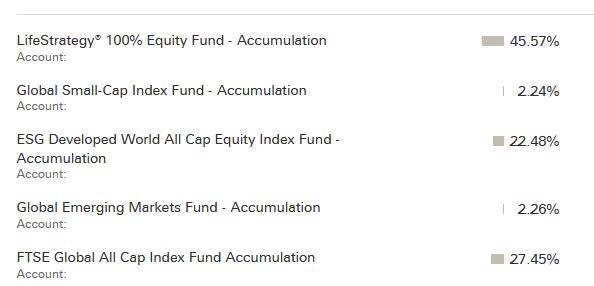

>>8628 I can also recommend Vanguard - it's a great platform. LifeStrategy 100% equity acc has been killing it for me - on about 28% returns atm (so that's a jinx)

>>8626 >Might instead just put it all on FTSE250

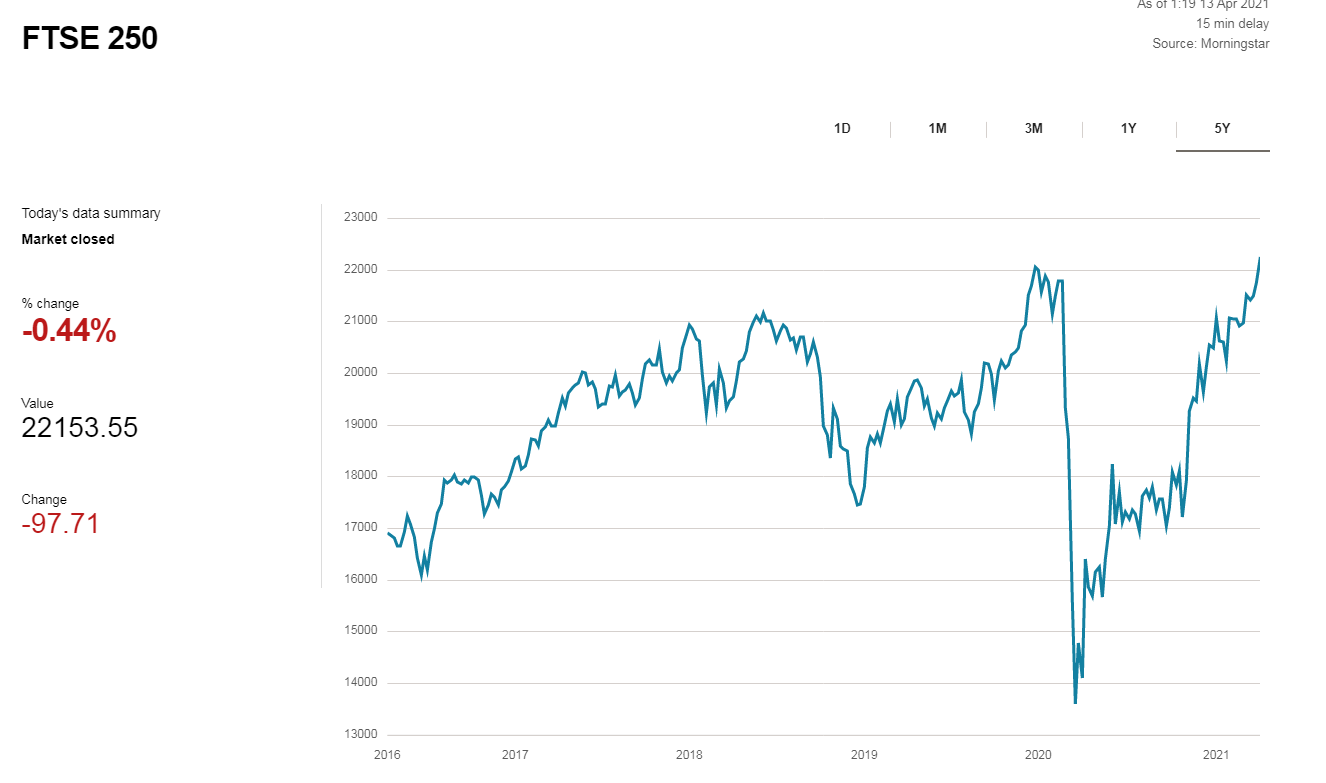

In a blind rage that I will never be able to afford a house, I wanted to buy 0.5 Bitcoins for a little over 20 grand, but it turns out my app has limited me to £3000 transactions. In doubly blind double-rage, I have just invested £5000 in a FTSE 250 tracker fund. I assume that's what you meant. I should really have checked.

It's a good thing I still have like 20 grand left over, so I can theoretically afford to lose the many thousands I have just thrown at the economic roulette wheel, more or less with my eyes shut. Anyway, I'll let you know if FTSE 250 was a good idea.

As for the 250, I think there's still some room for growth in the UK internal market; not least as we're doing rather well with Covid compared to Europe and got Brexit sorted which had held down UK investment (FTSE100 is larger more international companies). I would still recommend spreading your bets though, common wisdom is actually to do one of two things:

1. Use a global tracker but I'm more inclined toward developed economies at the moment and I don't invest in dictatorships.

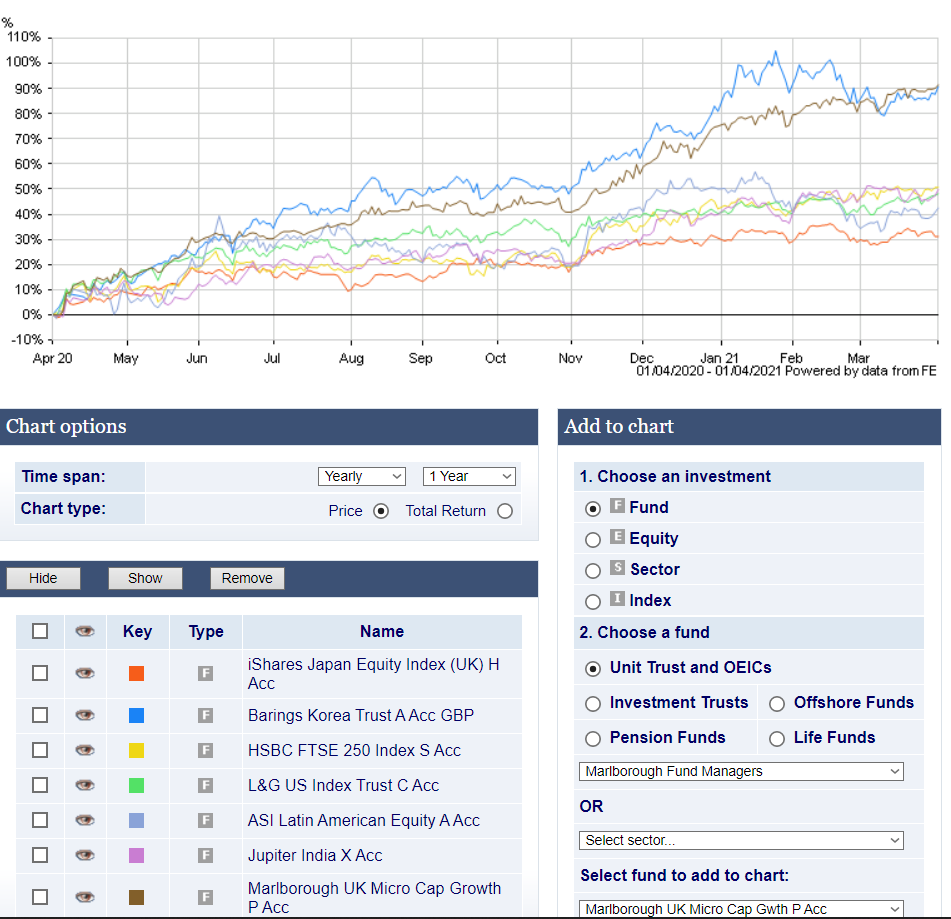

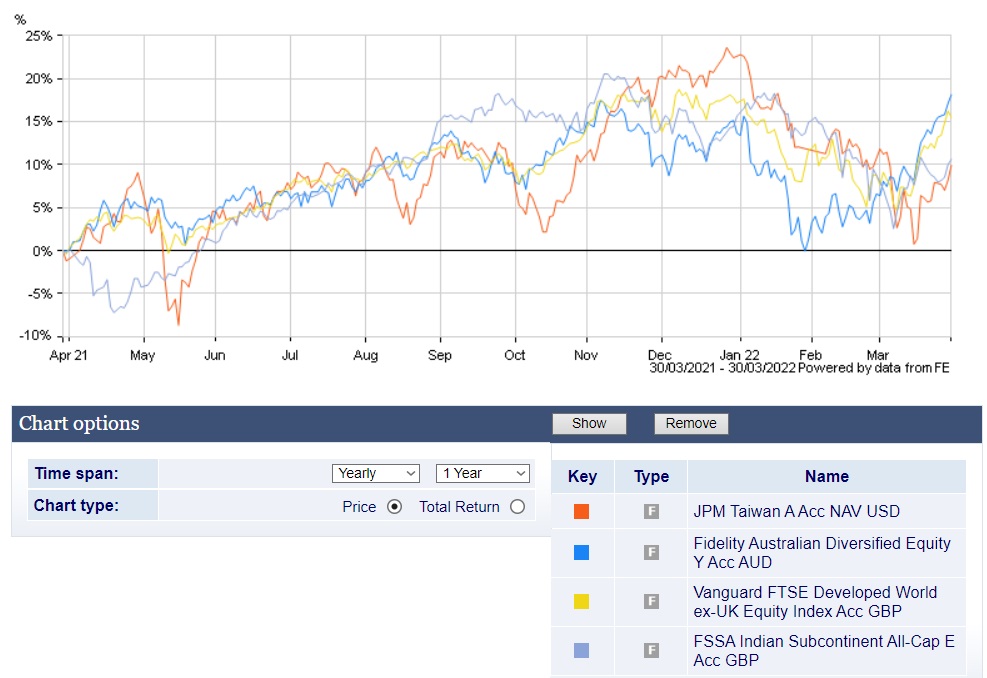

2. A US tracker or two is recommended but from experience you tend to just have general US on offer - you can see from the picture that the US has been the second best tracker which is about to overtake the FTSE250 and, let's be honest, the US is always going to be a better bet when it comes to the recovery. The economy is also sufficiently large and integral that you can get away with only investing in the US.

I like to have a foot in Japan because it can at times be counter-cyclical which stops some blood-red days but it's not a growth economy so you're just having peace of mind. Also You really can take a bigger risk with your cash, at least until the third quarter when everyone expects to see SHTF as governments realise they have no money and no reason to keep the life support on the economy.

>>8715 Yes, at a minimum your tax free amount but this can be a solid 90% of your portfolio (diversified across a number of indices) with your 10% on get-rich-quick bullshit. If indices collapse then we've all got far bigger things to worry about and you can now get that house with some mere judicious swings with a cricket bat onto someone's melon.

>>8717 >Yes, as a rule an index tracker will almost always beat active investment by a hedge fund over the long-term. There's a famous bet on the matter

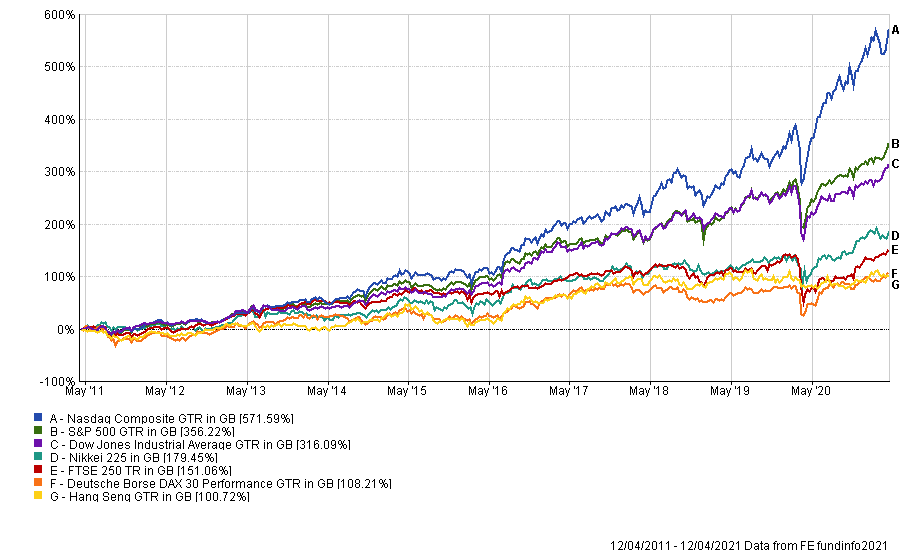

Going off on a tangent here, but it always bugs me when people use US-centric research when it comes to investing over here. It happens a lot on r/UKPersonalFinance.

Talking about hedge funds is almost entirely irrelevant when talking to a British investor so comparing how US hedge funds have done against the S&P 500 doesn't mean a great deal. It is fairly well known that it is much harder for active funds in the US to outperform compared with how they fare in global markets.

Do you have any research comparing UK active funds against the FTSE All Share, particularly those with the objective of beating it as not all active funds will have that aim, or comparing global active funds with a global equity tracker?

>>8718 >Do you have any research comparing UK active funds against the FTSE All Share, particularly those with the objective of beating it

Not on similar terms because no fund will take up a bet that involves undermining their entire business model. Buffett-Seides only happened for the publicity.

In terms of actual research a cursory google gave me the usual conclusions you would expect, UK active funds outperformed in the volatile 2020 market but that the 10 year is still a majority passive world. That summarises the idea of ordinary days as good for passive and extraordinary for active:

Overall that again calls into question the high-fees for active managers, especially once everyone has copied your successful buy-high, sell-low strategy.

>>8717 Me again. I have just done some very rudimentary research into whether or not it was a good idea to sink five Gs into the FTSE 250, and by the looks of things, I did so when it was at its highest point ever, or at least since 2016. It might grow further, of course, but I suspect my brilliant plan that it will all double in the next two weeks might not be as brilliant as I thought.

>>8721 >my brilliant plan that it will all double in the next two weeks

Lad, it's a tracker of the 101-350 largest companies on the London Stock Exchange. This is defensive investing where the object is to get solid returns for a lower diversified risk, that's what index funds do by allowing retail investors to own a piece of everything for (hopefully) low volatility growth. Also the fees are cheap which I like because I'm a tight-fisted ogre.

I strongly suggest you both read up and also lower your expectations before you lose everything on magic beans.

You need to think long term, that's what tracker funds are all about. Will you lose money tomorrow, next week, next month? Probably, maybe. Will you lose money over the next ten or fifteen years? Probably not, and you'll be slightly to mostly better off as compared to it sitting in an savings ISA.

Less than a week until the new year. What are you going to put money on?

I'm thinking of continuing on a west-focused portfolio given events over the past few months have shown the advantages, probably to opt for an Aussie fund in AUD given commodities still seem like a good bet and the Australian economy might be finding its legs again (until commodities fall). Taiwan could be interesting given how hard value has been hit in recent months but I have my doubts about it maintaining its position in the semiconductor market.

>>9217 > Less than a week until the new year. What are you going to put money on?

"Green" stuff. For my own conscience and because I think money will pour into the sector for decades to come, as the weather gets crazier.

Specifically:

- SSE: they build and operate lots of power plants, transmission lines, etc. Still some gas plants, but they are ramping up the renewables in a big way. They have a PE ratio of ~20 and a dividend yield of ~4.5%, so they are kind of a value stock I guess. I'll put £10k here.

- Agronomics: high-risk cultivated meat startup investment trust. I put £5k here about a year ago and the share price has not moved... but the net asset value is 200% higher, so this seems good value (despite Jim Mellon's extortionate fees). I'll put £5 here.

- The last £5k: maybe ishares global clean energy ETF... but this has a lot of highly valued stocks and may have further to fall, so I'm holding off for now.

>>9250 >Agronomics: high-risk cultivated meat startup investment trust. I put £5k here about a year ago and the share price has not moved... but the net asset value is 200% higher, so this seems good value (despite Jim Mellon's extortionate fees). I'll put £5 here.

If you want my top-tip, you'd invest in something that's going to make money. I've been looking hungrily at SSAB which has been making green steel, even if this will likely be a counter-cyclical bet.

You're nearly a month late anyway, I put my house money into a cheap fund looking at US Small companies and made a small profit already. I may shift that into UK nano companies as we have some smart lads in this country working on applications so long as they're able to switch the kettle on.

Another new year for those of us foolish enough to still be in the casino. What are you thinking for this year?

I've had some success with Swedish stocks in 2022 so I'm going to put my 4k Lifetime ISA allowance into a Nordic fund and hope I'll at least not lose money. For everything else I'm looking at playing things as boring as possible with an eye for opportunities. I think Microsoft will see some growth this year on the back of AI and it starting to challenge the dominance of Google in apps while Amazon will benefit from the enormous investment it's made in data infrastructure over the years.

Can't really think of anything in the UK that looks good despite being told repeatedly how undervalued the UK is. I could just still be mad about Truss and Kwarteng though.

>>9652 I do very minimal investing; I have a stocks-and-shares ISA with the FTSE 100 and FTSE 250 in it. Based on past graphs, the FTSE 250 does quite well every couple of years, and I have been absolutely haemorrhaging money on it for several years now. I know I sound like a gambler here, but surely it's due a year where it finishes 30% up rather than 30% down.

>>9659 I've heard many arguments that the FTSE is criminally undervalued but I have absolutely no idea why you would make it the sole constituent of your portfolio. It's not that I think you should only invest 2% in it as the share of global GDP but you can already see it's an unstable way to invest even with the 100's global focus.

I like to think we're on the arse-end of the bear market but even then you know we're liable to be the most sluggish of the G7 and there's plenty of deeply integrated economies abroad whose prosperity will be our prosperity if you're being nationalist about it.

>>9652 > Another new year for those of us foolish enough to still be in the casino. What are you thinking for this year?

Probably a combination of moving some stuff into an ISA to avoid CGT/dividend tax increases, topping up existing holdings, and an ultra-short bond fund (for the house deposit in the LISA).

Last year I bought:

- £5k UKW: 8.5% total return as of today

- £5k SSE: 6.9% total return

- £6.5k SMT: -10% total return

- £5.5k ANIC: -24% total return

> I like to think we're on the arse-end of the bear market but even then you know we're liable to be the most sluggish of the G7 and there's plenty of deeply integrated economies abroad whose prosperity will be our prosperity if you're being nationalist about it.

I think the key point about FTSE undervaluation is that many companies have revenue and operations globally and just have a lower valuation because they are listed in the UK rather than the US. An example mentioned a lot is BP (PE of ~4) in the UK vs. Exxon (PE of ~8) in the US.

I suddenly need to care about this stuff. I've been enrolled in my company's sharesave scheme for the last 3 years, it's matured and the shares are nearly double the grant price, so I'm holding a bunch of shares in a US company. About £30k - which is nice (from an £18K spend).

Can I just dump them into an ISA then swap them for a fund of other shares? It's not that I don't trust my employer, but eggs, baskets, not keen on it all vanishing for some batshit reason.

And then how do you get spendable cash out? I've got a loan to pay off in a couple of years, which this would cover. I'm assuming there's capital gains tax to pay - when? where? I should probably bother the bloke who used to do my accounts when I was ineptly running my own Ltd.

I do like the idea of money, but I'm so far out of my comfort zone here.

My broker has been hammering me with ads that the tax year is almost up. I don't think I've had that previously, probably a sign that the market is hungry for retail cash.

What are you two thinking about for the year ahead? I've made a bit of money off the arms and cybersecurity industry lately but my plan was to jump dump a big amount into the S&P this year. But then again, the magnificent 7 driven market is looking quite top-heavy and we've already seen a divergence. Maybe this will be the year that the undervalued FTSE will start to rise, unless Rachel Reeves does a Kwasi?

No new purchases next year. I have some shares outside of an ISA for historical reasons, and will be moving it inside to avoid the new CGT/dividend allowances.

I'm currently working through an umbrella, but also had a client who I invoiced direct (at their insistence). I've also had to pay for a replacement laptop, so put in a claim for relief on that as well as the usual £6/week. My adventures with HMRC so far:

* The umbrella is missing from my current year record. I filled out their online form giving the name, PAYE reference, payroll number, and a suitable start date. HMRC sent me a letter requesting that I provide them the name, PAYE reference, payroll number, and a suitable start date (with the PAYE reference stated at the top).

* They appear to have not queried the directly-billed income, which I wasn't expecting since despite consisting of at least half a dozen invoices they happened to total exactly £6000.

* They have demanded I provide receipts for the purchase, and evidence that I need it for work, along with evidence that I'm not working from home by choice. This is despite them previously having publicly stated that no evidence is required for the £6/week thing, and having previously accepted a similar claim for a society membership without question.

I have no idea how to deal with any of this, most people I know that make deductions for these things typically don't have to provide the receipts in advance (though need to retain them in case of an audit), and don't have to provide any justification for their claims. I'm with an umbrella specifically so I didn't have to go down the SA route for what could have been a couple of years, knowing that once HMRC put you on SA they have the right to keep you on SA forever, and so that I didn't have to deal with payments on account or having to find lump sum underpayments rather than having it done through coding.

I find it difficult to explain to people what my actual status is, since I'm effectively working freelance with very little SDC, and set my own rate, but courtesy of the umbrella I get payslips and a P60. This was a bit of a pain during COVID, because I wasn't entitled to furlough payments but because I'd started this arrangement at the end of 2019 I wouldn't have had a SA return at that point even had I not made the choice to try not to subject myself to it.

Though I guess I should have expected this, given that a year or two ago I went to my mailbox one day and found both a letter from HMRC demanding around £100 in underpaid tax and a cheque for around £100 in overpaid tax.

Not long now, lads. How will you be dodging the tax man investing this year? I'm not sure what's a good story to tell, maybe I'll use my ISA to put some money in Eurotech.

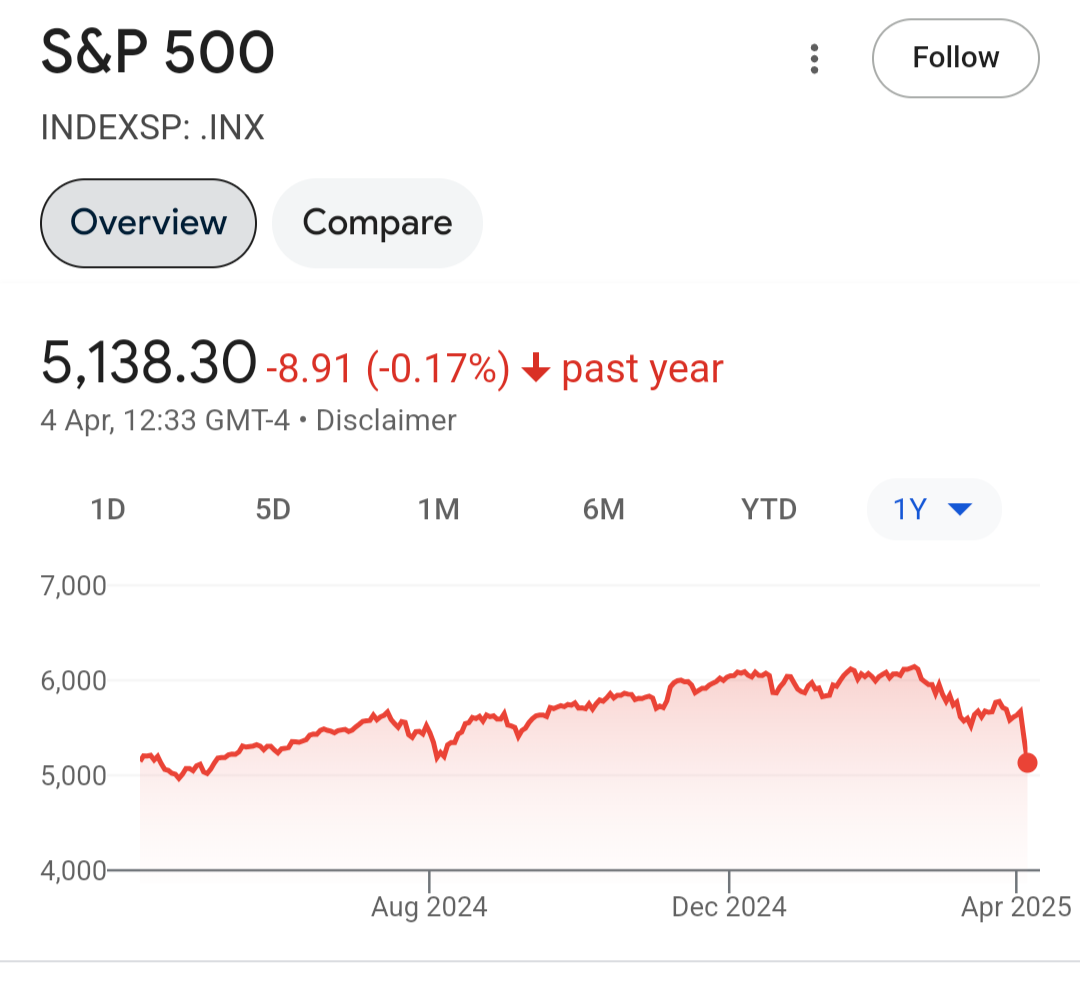

>>10054 My SIPP has dropped from £70k to £58k in a relatively short period of time, so I've chucked a couple of grand in to double down on my iShares S&P 500 Information Technology ETF.

>>10057 Potentially, but how will you know when the prices have dropped as low as they can go? The biggest shares are notoriously overvalued, so if they drop to a “reasonable” price, they have a long way still to fall. But at the same time, Donald Trump could U-turn on these tariffs and cancel them all and everything could be back up again this time next week. The hard part is guessing what’s going to happen next.

>>10057 If you bought into an S&P500 tracker now it'd roughly be the same price it was a year ago. It's a drastic fall but, in the grand scheme of things, I wouldn't go overboard about it.

The reason markets tend to fall like this is because the worst thing for share prices is uncertainty and when people don't know what's going to happen next. It happened immediately after Brexit, at the start of Covid, when Liz Truss had her mini-budget and it's happening now with Trump. Businesses can deal with bad news and plan around it. They can't deal with uncertainty when nobody has a clue what's going on. It'll stabilise sooner or later.

This problem is more fundamental than that, do you think the average investor knows what the supply chain of a company is? A company might know that all of it's suppliers are in the US but it doesn't know where it's suppliers suppliers are. It is entirely possible for an object to have previously crossed a border multiple times as it makes it's way from raw materials to components to complete products. It doesn't take many sprockets and widgets having doubled in price that you cannot produce a 'domestic' product for less than a foreign made one even with a final tariff on it. The entire reason free trade is supposed to stop wars is by creating interdependence. The fallout out from this isn't just uncertainty. It raises questions if certain businesses are even viable anymore but no one really knows which ones will fail.

If Classwarlad is watching then this is phenomenal timing for moving money into this year's ISA allowance. A fantastic outcome for medium term tax avoidance in the UK.

The interesting thing is the level of madness this involves, assuming Trump doesn't get defenestrated or suddenly back down then it seems like a criticism of Elite Theory that his first term didn't deliver.

>>10068 I think most people are pointing to the 1982 recession so it might be a bit more serious. Maybe we're looking at a 1970s stagflation in which case this might be the time to start looking at bonds again.

Most people are not looking at the big enough picture, and they are not nearly thinking mental enough. People have sort of started taking Trump seriously as though he basically knows what he's doing and we just need to wait and see how it plays out.

It's much worse than that. He literally wants to crash the dollar, he wants to destroy the dollar's status as world reserve, he wants wages for Americans to fall, he wants people to lose their homes. Then he can bring all that precious industry back because it will be just as cheap to pay American workers as it is to pay third worlders, in his mind.

He has taken the race to the bottom very seriously.