Mods are asleep, post budgets. Don't forget to comment on budgets and suggest budgetary improvements.

Some explainers for mine:

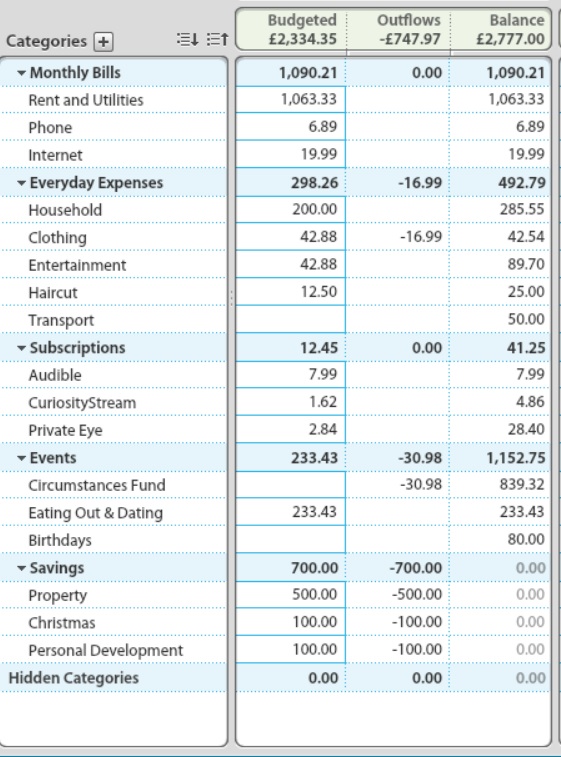

-Savings go off budget.

-I budget an £800~ fund for 'circumstances' i.e. odd unexpected costs.

-10% of my budget is for dating but in reality, I get two takeaways and then the rest goes into savings.

-Christmas seems excessive but I'm putting £100 because it's a round number I can put into an investment fund.

I don't really take holidays because I'm saving for a home but if I'm visiting my parents then I'll just raid my dating budget. I'll probably start letting it accrue soon rather than it going into savings so I can see the world/mates or so otherwise be ready for the massive amounts of money relationships can drain.

I don't do budgeting; I just don't spend money until I have spare money, then I can spend that without paying any attention to numbers. My life is far, far too dull to ever spend a lot on anything. I never go anywhere, and I only replace my kitchen sponge every few months because that's how long it takes a sponge to get completely worn through with a hole like a donut. I am basically a real-life Scrooge, except much poorer and much less willing to be woken up in the middle of the night.

If you want my personal financial situation:

For a long time, I had no savings at all, just a current account with all my money in the world.

Last year, I invested in a tracker fund. That now contains around £11,000, while my current account still contains around £22,000 that I can spend on whatever I want (except a house, because you know what it's like).

My rent and bills are less than yours; I save between £500 and £800 a month that just doesn't get spent unless I want something, and even then I probably talk myself out of buying it. My entertainment budget is zero unless that includes pubs.

>>8814 Tell me more about this £19.99/month Internet bill. I get cruelly bummed by Virgin Media every month. It's a good service, but when they take £55/month for the exact same service, at best, as you receive for £20, I hate them anyway, the thieving vipers.

>>8815 You should give it a try, there's a wonderful feeling of security attached to knowing everything is priced together. It also means you can better police yourself to be even more frugal. I'd probably also recommended moving most of that 22k into some funds you're just burning money on inflation at the moment with the bank investing for you and taking all the profits.

My internet is through Plusnet, it's fast enough broadband for anything I use the internet for and I get a cheaper phone bill for it. I've used them for years as I've consistently had decent service through them anyway.

Mine is also pretty simple. I share with the lass, so I spend less than I used to, but from my side:

Rent: £285

Bills: £110

Internet: £25

Phone: £10

Netflix: £15 (I think. Prime is paid once a year, I buy/pirate everything else).

Monthly spending: £300 (I keep as close to this as possible, this is for food, petrol, drinks, just general day to day).

Everything else gets put into savings. £200 into the Help to Buy and what is lest goes into a Santander 123.

Maybe I'm just a tight bastard but having a monthly allocation for clothes and spending £200+ on eating out seems mad to me. Each to their own though.

>>8819 >Maybe I'm just a tight bastard but having a monthly allocation for clothes and spending £200+ on eating out seems mad to me. Each to their own though.

There's an internal logic to it.

My fashion budget is actually being shagged harder than entertainment (computer games, headphone etc) as I've been building up a wardrobe of more expensive items that will last years. In theory this should save me in the long-run by simply having things that are well-made and serve a purpose. Plus I'm a bit of a fanny.

I live in London so £200+ on dating isn't completely unreasonable, the excess when not being converted into savings, goes on trips and holidays which benefits from a rollover. It'll obviously fall considerably once I'm deep into a relationship but then so will my rent and food bills so it's like an investment.

50% of my gross pay goes into my pension. That leaves take home pay of £2300, of which:

- £685 on rent

- £210 on council tax, gas, electric, water, internet and phone

- £100 or so on food.

- £100 or so on car maintenance/insurance (depreciation is tiny because the car is so old)

- £40 or so on petrol

- £500 or so on other stuff

- the rest (£600 or so) into savings/investments.

>>8834 I do wonder if there's some formula for working this out in terms of pension contributions v. return on investment. It's probably exists but I'm stupid and lazy.

The tax savings would be the main benefit in salary sacrifice but the opportunity cost and time preference etc. seems pretty steep along with locking you into a particular retirement where taking it early can carry some outrageous costs. We're all going to take early retirement in some form and likely won't be making large contributions near the end once we have to work part-time, a significant sum of money for your 60s therefore seems like a rational thing to hold. I'm not working at 75 no matter what robotic exoskeleton you give me, society can get fucked.

>>8835 Let's say you have £10,000 spare to invest. If you put it in an ISA then that's £10,000. If you put that into a pension then basic rate tax relief will gross that up to £12,500 and if you're a higher rate taxpayer you can claim a tax refund of a further £2,500 to make the net cost to you £7,500.

If we assume no growth and you took it out the following tax year then with the ISA you'd get your £10,000 back. With the pension if we assume it was 25% tax-free and 75% at a marginal rate of 20% then you'd receive £10,625 back so that's an immediate net uplift of 6.25% for the basic rate taxpayer and for the higher rate taxpayer a whopping 41.67%. Most higher rate taxpayers are basic rate taxpayers in retirement and many also have their personal allowance to take advantage of as well.

Let's say you leave it and it grows by 10%. The £10,000 in the ISA grows by £1,000 to £11,000. The £12,500 in the pension grows by £1,250 to £13,750. You've achieved further growth of £250 just by choosing a pension over the ISA; again if we assume 25% tax-free and 75% at basic rate tax then that £250 additional growth becomes being £212.50 net better off. You can see how this could add up over the years.