How do we fix the housing problem? The whole market is a joke and weighs on the neck of anyone whose parents aren't rich like an anchor.

Talk of raising interest rates by a single percent could knock 20% off house prices (https://www.economic-policy.org/72nd-economic-policy-panel/rising-uk-house-prices/) but the factors driving low interest rates in the need to artificially pump growth seems unlikely to abate anytime soon and it seems like we just can't build possibly enough houses to possibly dent demand. It's like as a society we're just tired and out of ideas at this point.

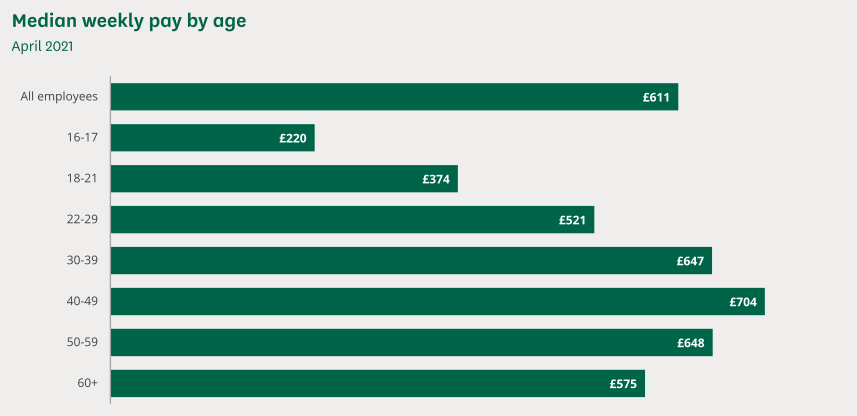

The average UK house price is £274,000. The median weekly pay for full-time employees is £611, so £31,772 per annum. That means a couple both on median earnings would have a joint income of £63,544. £63,544 * 4.5 = £285,984. A doddle.

The only people I know who moan about the housing market either live around London or have no financial discipline. Sage because we have a dozen or so other threads about this, all saying the same thing.

>>9263 >Move out of the south where most of the jobs are

>Get on Tinder and find a partner that earns X amount a year

Do you own a house? I guess that would explain why you are excusing what we have now.

>>9264 You don't have to move south to earn around £32k a year, especially with the rise of homeworking. Seeing as you'll need a 5% deposit you'd need a mortgage of c. £260k that means a couple earning an average of c. £29k each could afford the average house price.

Most people buying a house do so as a couple. I know a few people who've bought on their own and they tend to go for flats, which will be cheaper than the average house price.

I think you're drifting from the point of this thread, it's not that housing is (at the moment) impossibly out of reach but that the cost of housing is just absolutely outrageous even if you're buying a one-room shitbox. It's a significant weight on the real income that squeezes peoples wellbeing and the productive areas of the economy.

It's really not lad. It might look like the promised land up north by comparison to the south, but the price of a 2 or 3 bed semi comfortably exceeds that of an average earning couple's combined income in a lot of places, and remains only just on the cusp of affordable everywhere else.

People can get a back to back townhouse or whatever, but if you want to settle and think about having kids those sorts of homes (very little space, often right next to main roads, horrible air quality, and so on) are really not the environment you want.

No, you'll need 15%. Stumping up 30 or 40 grand is no mean feat and that's the main stumbling block people face. It's not the overall cost people can't afford, it's the ludicrous barrier to entry.

Ah I don't know why we're wasting our energy typing here, there's always one lad who's opinions sound like he's the nephew of a broadsheet editor and the closest he ever gets to reality is Channel 4 poverty porn docs.

>>9270 >Ah I don't know why we're wasting our energy typing here, there's always one lad who's opinions sound like he's the nephew of a broadsheet editor and the closest he ever gets to reality is Channel 4 poverty porn docs.

I'm trying to work out what combination of policies I'm supposed to wish for outside of bashing the heads in of the BTL community. It seems like so much depends on a magic wand that creates housing that will have it's work cut out for it from not only a rising population but an even higher rising number of households.

>>9272 >a magic wand that creates housing

It's a shame the government managed to lose theirs down the back of the couch or off the side of some oligarch's yacht or wherever it is that ministers hang out.

I mean, that's essentially what needs to be done, short of just enacting a slash and burn policy to the green belt and putting up a load of post-war style prefabs.

The trouble with the whole BTL thing is that they're not only essentially acting as scalpers, sucking up the supply before anyone else can get a look in and reselling it at over the odds prices; but that they're capable of having so much more leverage over an ordinary buyer looking for a home.

Let's say you find a house that looks perfect for you, it's just in your budget, and you put an offer in. You might have been sensible and accounted for having to go a bit higher- But adding an extra ten grand on to the offer, as an individual buyer, means you've got to come up with another two, for, ten grand for your deposit, and you're probably already pushing the limit of what a mortgage would cost you. But a BTL investor who's planning to buy it interest-only? It means fuck all to him. It will barely touch his repayments.

I really think banning interest only mortgages is the solution. I mean think about it- In what other market does such an insane financial construct exist?

Every local authority employs people whose sole job is to stop people from building things. They spend all day coming up with spurious arguments like "you can't build a housing estate on that plot of derelict land, because it doesn't have a bus stop" or "you can't build a block of flats there, because someone says they saw a newt". String 'em up.

>>9274 >I really think banning interest only mortgages is the solution. I mean think about it- In what other market does such an insane financial construct exist?

Bankerladm91 reporting in. Credit default swaps. Binary options. Compound options. Look-back options. There are plenty of things out there that are far worse than interest-only mortgages. Unfortunately, property ownership, and BTL are feted as a grand money-making scheme in the UK and US - and a very large part of our elder population are relying on rapidly growing house prices for social-care. You have to solve those inter-dependencies I think.

I've owned property in the past, but right now I rent and am very happy with it; much of Europe rents - 48% of people rent in Germany, for instance. I have a five bedroom house, with three gardens, a garage, two sheds (!!) and a driveway (which is going to be very handy for when my Tesla arrives) in a relatively posh part of Hampshire. I pay less than a 2-bedroom flat in Grenfell Tower was going for, before it burned down. The dirty secret of the property market is how long it can take to sell a house. I've teenage kids who are leaving school, I might buy again when they're gone and me and the missus move somewhere even greener, I might just rent forever.

My roundabout point ladm7s is, don't get sucked into believing that property ownership is all its cracked up to be - there are other ways. Put more money in your pension and retire early, its a better investment than housing.

1 - I should also declare I no longer work in a bank - I'm in the NHS now, and I get paid more, but that's likely to really trigger everyone.

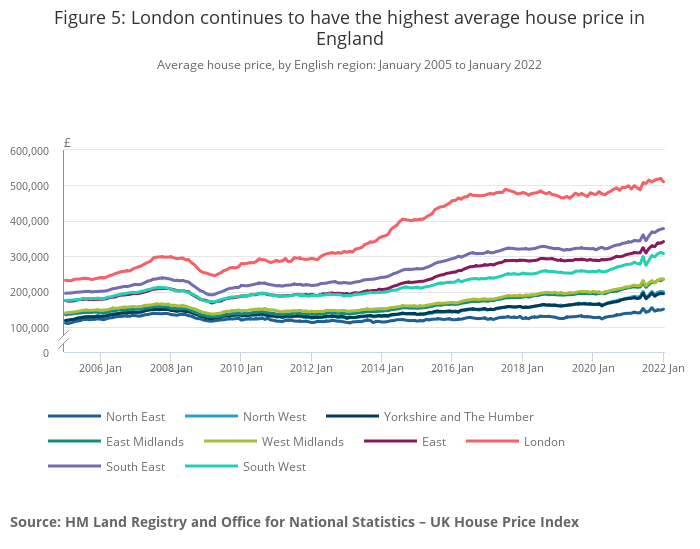

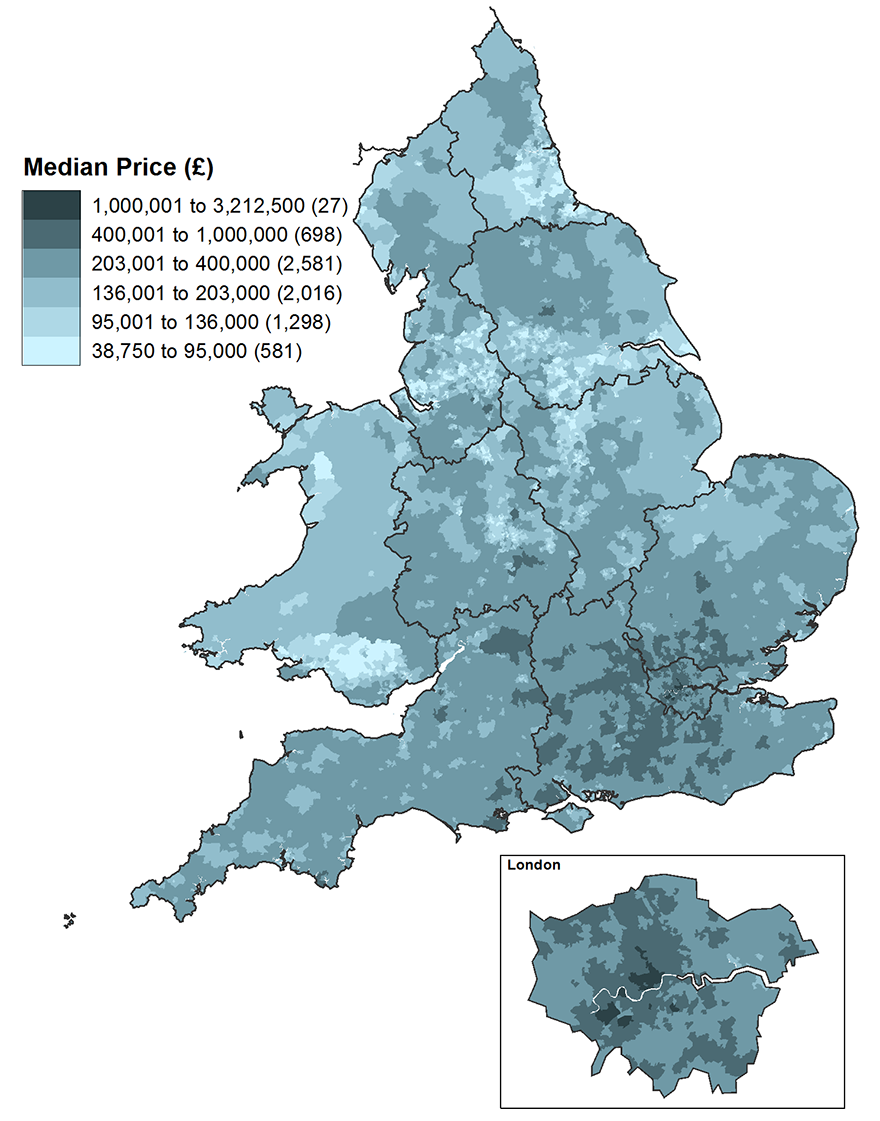

>>9265 What on earth happen in 2014 to cause East to diverge from SouthWest?

Everything else just seems to scale the same with that lunnun being a bit madder.

The key, as far as I can tell, is to stop anyone from owning multiple houses. There are plenty of houses in this country; we know this because we rent them. We just need to find a way to make the owners sell them.

My own proposal for how to do this is a threefold plan of increasingly militant, but wholly nonviolent, steps:

1) Have a list of who owns every house in the country. The government, yes, the actual Conservative Party, are already introducing plans to do this, so it can't be that extreme. Also, make it so every house must be owned by a person, rather than Anon Ltd. Housing companies will have to put the houses in the names of their CEO, but nothing else needs to change. This will have the added benefit of massively reducing corruption.

2) Cap rents. This means that if, hypothetically, step 3 is going to financially harm professional landlords, they cannot pass the costs on to their tenants. This will make the job of landlord much less attractive, but it's still an entirely reasonable policy. We might not even need step 3 if the landlords can guess where this is going.

3) Anyone whose name is on the homeowner list more than once, gets charged an extremely punitive tax. To begin with, that will be 10% of the value of each additional home they own, per year. That tax money will then be used to hire lots of people, creating jobs, to go around every house in the country and revalue it. Once it has its much higher valuation, due to houses being more expensive now, the tax will increase accordingly. Anyone who is rich enough to have a second home in a holiday area can keep it, but they'll need to be even richer than they already are. Those who aren't that rich can sell their holiday homes. In the event that this incredible plan still doesn't work, let's just increase the punitive tax to 15%. Or 20%. Or 40%, or 50%. If your council tax becomes £400,000 a year on your second home, fantastic. I don't give a fuck. It's this or we hang you. Take the hint.

Obviously there will be some complaints about pension companies having bought all the houses. But we already have a pensions crisis looming. Most people will not be able to live on their pensions when they retire in 10-40 years. The pensions companies are fucked either way. They're not on our side. Fuck them. Other housing companies that rent out hundreds of flats and houses will complain too, that they're going to fold overnight. Good. The job market is looking great for everyone right now; just work somewhere else. Thanks, Boris; you have enabled us to implement this plan of national rescue. And there will also be complaints from old boomers who want to invest their life savings somewhere. Again, that's wonderful. Invest your money in the stock market. Put it into the British economy. Think of the massive increases we'll see in wages, and in business growth, and in employee productivity, and general job satisfaction. It'll be a golden age. And we won't need to hang a single person from a lamppost unless they really insist on it. It's the perfect plan.

Financial products are a whole different thing because that's a fictional market in the first place. Of course you can have barmy buy-now-pay-never schemes when the whole concept is made up from the word go. But houses are a real life commodity, bricks and mortar. They're what people live in.

You wouldn't buy a car or on interest only finance, because it's never going to be worth more than when you bought it unless it's something really special. We need houses to return to being that kind of commodity, a sensible practical good valued on its utility as a home, not as a speculation vehicle.

Anyway the reason I suggest banning that is because that's how the BTL lot always finance their property empires. You pay next to nothing, you're not really the owner, you're just a middle man between the bank (the real owner) and the tennant, but you're laughing because you know the thing will be worth more than when you started no matter what.

The banks won't lend ordinary buyers this way, only investors, which is another thing that seems a bit backward to me- Surely letting a young couple get their foot on the ladder with a really cheap mortgage, then selling the house for a bit more later on, should be what that type of mortgage is ideal for? But no. Can't take risks on the people who actually need a home to live in, only the scalpers who are keeping the market this superheated to begin with.

Which cuts to the core of the problem really as with most things. The people who are making loadsadosh out of the state of the current market would really rather keep on making loadsadosh, and they couldn't give a fuck what long term effect it has on our economy.

>>9280 >Can we do a little bit of hanging? Just Kirsty and Phil, to send a messsage.

If we're really going to send a message, then fuck Kirsty and Phil; BorisB got two and half years. Stick Katie Price in jail for her shameless exploitation of the legal system and the way she exploits her deeply autistic child. Let's kill all the influencers and then we can start on the property porn.

Leave your mission creep out of it spooklad, this movement will not be compromised so easily. This is a single issue party. We don't care about bipoc disabled trans representation. We have concrete demands and our methods will get results, because the establishment can't just safely ignore it.

Now start taxing Buy to Let landlords or else Kirsty loses another finger. We're hoping we don't have to get to her toes.

Fuck it all, I think the only way we're digging out of this mess is nationalising the banks and making them non-profit.

Looking at most mortgages, you on average end up paying half the overall value of the mortgage in interest. On a mortage for £200,000 you end up paying back £300,000. That's a hell of a profit margin to be extracting out of people who already have their finances squeezed; but more importantly, that tells me lots of people who "can't afford" to buy, really can afford it, if only the banks weren't taking such a massive cut.

Mortgage rates have been at record lows since 2008.

The problem with the housing market is simple supply and demand - the number of houses available hasn't kept pace with the number of households. The government could loosen planning restrictions and spark a massive housebuilding boom, but they don't want to because so many people are reliant on property investments for their retirement, either directly through buy-to-let or indirectly through REITs. Cheaper rents and lower house prices would be almost entirely offset by the cost of propping up pensions.

>>9286 Between April 2013 and September 2021 a total of 346,656 properties were bought using help to buy loans, with the loans accounting for £21.4bn of the £96.4bn overall properties bought with help through the scheme.

As the government is effectively buying a percentage stake in these properties until the loans are paid off they've got an incentive in keeping property prices rising.

Record lows is all good and well, but interest is a percentage. Which means that the more the loan is worth, the more you're paying. And what do we know? House prices are higher than ever. Banks could afford to cut interest even further, because they're still making more money than ever before, record lows or not. The profit they're making is obscene and I don't know why you would even try to deny or defend that.

Supply and demand is obviously a factor in the long term overheating, but if we want short-term measures that could help more people get on the ladder, this is one of the many areas we could put slack into the system. The amount of money people get rinsed out of for no good reason is the other half of the issue.

We need to get it under control for the sake of the economy as a whole. This country's prosperity currently floats on nothing but the real estate pyramid scheme, and it's already starting to bite us in the arse. An inflexible property market makes it harder for workers to move where the jobs are. That makes it harder for businesses to recruit. It starts to strangle the economy itself.

There's a young lass at work who's jut started a job at one of the Sheffield hospitals, and she's moving down there. Decent job for a biomedical grad, she can afford to live well in that city, but she's looking at at least £900pcm for rent. Partially that's just her being a bloody idiot and spoiled middle class tart who's scared of the more affordable areas (somewhat justifiably, she wouldn't last two minutes in Manor Park) but it's still beyond absurd.

I was laughing at her about it, because after deducting the cost of housing and bills etc from her wage, she'll have less money left over than I did as an apprentice on £120 a week 7 years ago. But I suspect in a few years when her youthful optimism and naivety wears off, she is going to be very pissed off about the future she has in store for her.

>if we want short-term measures that could help more people get on the ladder, this is one of the many areas we could put slack into the system

Mortgage rates aren't stopping people from buying a house, deposits and lending ratios are. We could relax lending criteria and give people 100% mortgages on 5.5x income, but that's how the 2008 crisis happened. Mortgages are very cheap at the moment, but they're likely to become less cheap at some point in the next 25 years; we have to lend with this in mind, otherwise we'll inevitably end up with horrible negative equity traps. It doesn't help anyone if you lend them more than they can afford to sustainably repay and set them up for failure.

We need to build more, but we can't build more. That's the fundamental problem. The only easy answer is "fuck the old", but the old outnumber and outvote the young.

>>9289 You only need a 5% deposit if you can borrow the rest. But most people don't earn enough to borrow 95% of 250 grand. Changing the multiple of your income that you can borrow would sort this out. However, everyone would try that and it would just drive prices up further unless more houses started appearing on the market. Which they don't. It's entirely an issue of supply (and the location of that supply; most people probably could save up for a house in rural Scotland, but that's no good for most people).

If someone can afford to pay a mortgage that comes out as £300,000 in total, they can afford to buy a £300,000 house, the only difference is the bank making less profit.

Same way a rented who's comfortably paying £750 a month in rent could afford a mortgage of £750 a month, if only anyone would let them.

I don't understand where this euphemistic language about lending "more than they can afford" comes from, because the evidence is right there that they can afford it, because that's already how much they have to pay.

>ooh but we can't possibly 5.5x because the 2008

Nonsense, this is part of my point. If I earn £25k, I can get a mortgage on a house worth £112,500. Right? But the total amount payable on that mortgage, however, is nearly £200,000. So never mind 5.5x, I am actually paying 8x my income on that mortgage. Eight times. That's two fours. One fat lady. Eight (8). Do you see what I'm getting at?

I'm not saying it's necessarily a good idea to give out mortgages so highly leveraged, but what I am saying is that this line of reasoning doesn't add up at all.

>We need to build more, but we can't build more. That's the fundamental problem. The only easy answer is "fuck the old", but the old outnumber and outvote the young.

Which is exactly why I'm proposing different ideas. What you're saying appears to just be "No, there's nothing to be done about it, its absolutely impossible. It's such a shame but I'm afraid there's no conceivable way it can be changed."

>>9291 If you borrow 112 grand and pay back 200 grand, you haven't remortgaged for a better deal later on, which you are expected to do. The numbers are still scary, but they're less scary once you shop around for better deals each time you reach the end of your fixed term.

And the rules for deposits have to screw over some people, otherwise everyone would be able to buy houses, demand would go up, supply still wouldn't, and prices would continue to skyrocket insanely like they're doing now. But even then, if we build more houses, landlords will buy them all and you'll still be fucked. A second-home tax would help with this.

>>9291 >But the total amount payable on that mortgage, however, is nearly £200,000. So never mind 5.5x, I am actually paying 8x my income on that mortgage. Eight times. That's two fours. One fat lady. Eight (8). Do you see what I'm getting at?

What exactly do you think happens when you borrow money over a 30 year period? Even low interest rates will stack up when you're talking about a three decade term.

Naturally the stock still needs to go up, but that's a longer term problem. Houses can't be built over night, but interest rates could be slashed over night.

Lenders are already rich enough, I don't know why you lot are on their side for some reason.

>Which is exactly why I'm proposing different ideas. What you're saying appears to just be "No, there's nothing to be done about it, its absolutely impossible... Are you a landlord, or just a Tory MP?

You're proposing one absolutely terrible idea and dismissing all the reasons why it's terrible out of hand. With the current state of the economy, banks are effectively paying you to take out a mortgage because the interest rate is significantly less than the rate of inflation. Mortgages are incredibly cheap and have been for over a decade; any attempt to increase affordability through relaxing lending criteria would inevitably increase risk, because the interest rate isn't likely to remain at record lows forever.

Reducing interest costs won't make housing any more affordable, because it won't change the balance of supply and demand. If people can borrow more money more cheaply, prices will inevitably rise because the same or a greater number of buyers will be bidding against each other for the same finite pool of housing. It's like a game of musical chairs - someone will always lose if there are fewer chairs than people. You can give all the players steroids and amphetamines to make them run really fast, but it won't change how many people are sitting down when the music stops.

"Ooh but we can't possibly 5.5x because the 2008" is an incredibly glib way of dismissing the worst recession in nearly a century. The economy had only just recovered from the 2008 crash at the start of the pandemic. The consequences of that crash weren't just numbers on a screen, they were real businesses going bankrupt, real people losing their jobs, real tax going to bail out banks. We do not want to repeat that. Pumping more money into the housing market doesn't change the basic dynamics of supply and demand, but it does have a massive distorting effect on the rest of the economy.

The US effectively nationalised a large proportion of mortgage lending through FNMA and FHLMC. It has not worked out particularly well for anyone.

>You're proposing one absolutely terrible idea and dismissing all the reasons why it's terrible out of hand.

Because you haven't actually given any.

>With the current state of the economy, banks are effectively paying you to take out a mortgage because the interest rate is significantly less than the rate of inflation.

Now we're getting somewhere. This is a more sensible reason. So what you're telling me is that banks actually lose money on mortgages? Why the fuck are they doing them then?

>risk

But there is no risk. Absolutely none. If someone defaults on their mortgage, you repossess it, and sell it at more than the original value, because houses only ever go up. Unless there's a crash, in which case fuck 'em anyway, they've been asking for it for 30 years.

Maybe I am being naive about it because I'm a dirty peasant who just doesn't get why money works they way it does. But I'm also not thick, and I know lots of these cunts are making a lot of fucking money out of the situation. Stopping them from doing so would at least go some of the way to making the market more amenable to fulfilling the purpose it's supposed to.

>FNMA and FHLMC

There are a lot of other reasons that was a shower of shite, and mainly they're due to good old fashioned American corruption and lobbying and what have you. It wasn't a terrible idea in principle.

Moreover, 2008 was caused by the Yank property implosion, and had fuck all to do with ours; I can't imagine the British property market causing anything similar on a worldwide level like theirs did. Something something Bretton Woods global reserve currency innit.

>>9291 >If someone can afford to pay a mortgage that comes out as £300,000 in total, they can afford to buy a £300,000 house, the only difference is the bank making less profit.

>Same way a rented who's comfortably paying £750 a month in rent could afford a mortgage of £750 a month, if only anyone would let them.

>I don't understand where this euphemistic language about lending "more than they can afford" comes from, because the evidence is right there that they can afford it, because that's already how much they have to pay.

Because ultimately that person who can afford to pay £750 a month in rent can afford to pay that only until they retire, and that's the real affordability cap at the end of the day. The banks would be quite happy to have people in lifelong debt, but that's not an option for obvious reasons.

What doe that have to do with it? If it's more than they'd be able to pay off by retirement then yes, it's too much, but that depends how old the person is and how much they're willing to pay. But as it stands right now, the 4.5x figure seems fairly arbitrary- nudging it up to 5 or 6 times still results in easily affordable monthly payments for anyone working full time and younger than about 40.

More to the point, how the fuck are these hypothetical retirees going to keep paying £750 a month in rent after retirement, because they were never allowed to buy a house? Which also answers >>9295's question. Having your mortgage paid off and being able to live off a few hundred quid a month is the only way most people can expect a reasonable retirement age, and a reasonable quality of life in retirement.

It's the only reason I give a shit about ownership, at least. If rents are this out of control now, imagine what they'll be like by the time I'm 68.

>So what you're telling me is that banks actually lose money on mortgages? Why the fuck are they doing them then?

Securitisation and fees. The mortgage market is sufficiently competitive that there's almost no margin on a competitively-priced loan. The bank will make a bit of money on you if you've got a particularly crap deal, they make a bit of money on arrangement fees, but the whole business relies upon the fact that pension funds will buy up massive amounts of mortgage-backed securities.

Pension funds have truly mind-bending amounts of money and there aren't many good places to put it at the moment; the knowledge that the government will prop up the housing market make mortgage-backed securities tantamount to gilts but with better yields.

Mortgages are profitable, but the margins are incredibly thin and it just wouldn't make a meaningful difference to borrowers if they were run on a not-for-profit basis. Supermarkets are a similar example - Tesco might make large profits because the sell enormous quantities of stuff, but less than 3p of each pound you spend at the till becomes profit. Like most FTSE 100 companies, pension funds are the biggest shareholders in Tesco, so those profits ultimately end up going to someone's nan.

That's the thing you've got to get your head around. "The Banks" aren't an unknowable foreign entity and their profits don't get spunked on cocaine and superyachts. They are, like most stable assets, mostly owned by pension funds. You're not being ripped off by a shadowy cabal of billionaires, you're being slowly bled dry by millions of ordinary pensioners and soon-to-be pensioners. Taking money from big business doesn't mean taking money from a tiny elite, it means taking a bit of money from millions of pensioners. That is an immensely difficult political problem when the majority of the electorate are over 50.

>>9302 >Taking money from big business doesn't mean taking money from a tiny elite

But it can't hurt. It will encourage them to reconsider their choices. I can't fight back against pension companies, but the CEO of Santander can. This is how they play the game against us; let's make them join our team at least.

>>9301 nudging it up to 5 or 6 times still results in easily affordable monthly payments

As long as interest rates stay in this weird low state, and as long as house prices keep going up so interest only makes sense for people doing that.

If interest rates go up, a lot of people are fucked. That's what the affordability stuff is taking into account. If you have a mortgage, you don't get to tighten your belt, move in with your mates or mum. You're on the hook for repaying a huge amount. Get repossessed an you owe the difference, while still not having a house.

<old git mode>

I bought my house in 1997, right at the bottom of the dip in that graph, just before it climbs off into the top right. I had a 25% deposit, was borrowing <3x my salary. I still had to get my dad to guarantee the mortgage. Even when houses are as cheap as they get, you still can't buy the fuckers, because they're always priced to just over what most people can afford.

If house prices ever become affordable, they'll increase in price until they're not. Human nature, and people always wanting better housing, will see to that. Money's currently cheap, so houses prices are high. If money becomes expensive to borrow, houses will become cheap, and you'll still not get one. Shit, fundamentally, sucks.

The only people doing interest-only are BTL landlords and investors, because it's usually a more short term investment and they're unlikely to lose money on it, and those people already have other property assets that can be recouped if it does go bad. They categorically will not give them to anyone who's intending to actually live in the place (and rightly so, it doesn't make any sense in that situation and never did, it was always just kicking a can down the road.)

This is why my first suggestion in the thread was banning interest-only mortgages- The problem is supply and demand, but a huge reason the demand is oversaturated is thanks to BTL.

>If interest rates go up, a lot of people are fucked.

Right, so what is it that drives this, and why? What makes The Interest Rates this omnipresent and unavoidable force of financial nature? Why can't the lender just absorb that, since as we've established, they're already selling the mortgage itself at a loss. Surely that would just make the market even more dependable, and give the real customers in these pension funds an even more stable investment?

It never really made sense to me why when you borrow money on a house, they're allowed to say "Tough shit sonny Jim, it's worth more now, so now you owe us more" and not you being able to say "Tough shit sonny Bank, you agreed to lend me this amount of money, so that's the amount of money you're getting back." I mean it makes sense in terms of they're the ones with the power so they're the ones who set the terms, but from an abstract ethical point of view it's backwards.

>>9308 > They categorically will not give them to anyone who's intending to actually live in the place

So why do banks say on their websites that they do?

>>9309 and yes, it offends me, too, that ordinary people have to make this enormous gamble, and the downside is much lower for BTLers.

How to fix it, though, is beyond my limited brain. I'm sidelined now, plan to get old and die in this house, so I'm just an interested observer, watching this country (and some others) grind itself into a sad state.

Nah, it'll be fine. Soon, we'll have poorhouses / workhouses. They'll be called something else, but...

They do it for investors because those investors can easily just sell the asset to repay the remaining value, and that's what they do. If it's an ordinary person, they can't do that, because they'd essentially risk becoming homeless.

They used to do it because the assumption was people would always be able to trade up for a profit, using that to repay the original value while still having enough left over to put down a deposit on somewhere new, then everybody wins; but then the 2008.

I'd imagine if you're earning six figures and have enough to put down a huge chunk of the capital down as the deposit and only mortgage half of it, they'll still take a gamble on you.

Well there you are then. Comfortably out of reach of Average Joe and Jane Pleb, with their combined income of 50k. Easily affordable for John Propertyladder who's putting down fifty grand from the flat he just sold, to buy another one closer to the city centre he can charge a higher rent on.

>>9315 >Easily affordable for John Propertyladder who's putting down fifty grand from the flat he just sold, to buy another one closer to the city centre he can charge a higher rent on.

That's not what you do with BTL. You wait for property prices to go up and then remortgage your BTL to release the equity you've built up and use this as a deposit to buy your next BTL. You don't sell the first one.

That's the primary argument for me. I don't see any other way in which retirement is financially feasible, it's a ticking clock and a big source of anxiety for me. I know I'll be far too fucked to carry on working full time by my 60s. I can hardly be arsed now, never mind in another 30 years.

I remember having the realisation when I was about 25 (which I think, to my credit, is earlier than most people) and started doing responsible things like paying into a pension and an ISA for a deposit. I just want a home to live in that I can actually call mine. And Englishman' home is his castle and all that.

Improving renting with controls and protections and all that sounds nice, sure, and it would have made my 20s much more pleasant; but it's simply never going to give you the same freedom as owning your home outright does, and I would still have wanted to buy my own place by this stage of my life.

I see. Same principle though, you know what I mean. Having assets already gives you more options in acquiring future assets.

I see a lot of "tenanted investment opportunities" up for sale on Zoopla, though, so they must have reasons to sell. I've been wondering if it would be too horrible of me to just buy one of those and then evict the current tenants.

>>9320 Help to buy and stuff like that is meant to level the playing field a bit, though?

people with a big pile of cash are always going to have advantages, that's why they go to such lengths to acquire it. Stopping that will require quite a big change.

The equity loan version of it doesn't really help someone who couldn't otherwise buy, it only helps people who could already buy get somewhere a bit more expensive. So it's really just like the suggestion of increasing LTV rates and income multiplier.

The HTB ISA scheme was fairly good, but only if you started it well in advance, an the recent spike in prices and deposits soaring has negated much of the benefit it offered. The maximum amount they pay a bonus on is £15,000, but £15,000 is about the bare minimum you'll need for a deposit a lot of places in today's market.

The other components of it are just meaningless waffle. Shared ownership is a disaster waiting to happen and any mug can see it. The "mortgage guarantee scheme" that's supposed to ensure 95% mortgages remain available is just... Well, it doesn't actually exist, as far as I've been able to tell, because I can't fucking get one.

The "First Homes" thing sounded promising at first but when you read the fine print that too sounds like a con. You get to buy at a discount, but you have to sell at the same discount, so it could well turn out to be a trap. And besides that none of them appear to have actually been built yet.

And I mean even without all of that, just look at the website, and see if you can figure out how to actually take advantage of any of it. They can't even be arsed providing links to participating builders or an overview of locations.

>>9321 Help to buy has largely allowed those on above average incomes to buy above average properties by being able to use government leverage for an additional 20% deposit (40% in London).

It's helped people that would have been able to afford a property in the first place buy a nicer one than they would have otherwise.

>>9320 They'll have a contract. You can evict them when the contract expires, but you won't be able to move in until then.

I saw ground rent being sold once. Someone had a leasehold house and the ground it was on was up for sale, so you could buy it (it was about five grand if I remember correctly) and then let the ground rent roll in and make a profit after 20 years or so. I wondered if I could just increase the ground rent so much that the homeowners would be forced to move out, and they could sell me the house.

>>9325 Would you still want to buy if house prices were falling?

Would you buy now, or give it a while?

What if lenders were saying they wanted massive deposits to cover expected reductions in price?

As soon as house prices stop going up, you'll get to try to solve these questions and others, while just wanting somewhere to live. There will probably be a recession on, too, if that helps?

>>9327 If house prices were actively plummeting, then yes, I might wait to get a better deal. But they're not, nor have they been during any of the past economic crises. So it's kind of a moot point, and if they do plummet just as I buy one, then they'll still go up again maybe a year later because that's what happened in 2008. I won't have negative equity because the credit crunch only dropped prices by about 10%, and my deposit is more than that, same as anyone else looking to buy now. And my work apparently does massively well when there is a recession, so I'm not afraid of that either.

I'd still want to buy, but I think anyone would agree it's best to do so at a time the market is stable. However, the fact is you don't really get a say in the matter, you take the chance whenever you can afford it. Most people do not have the financial luxury of making this decision based on market fluctuations, and if they did this thread would not be relevant.

That said, if I were given my choice of alternate realities that will never exist, I think I'd still take the one where everyone turns into a furry and I get to shag slutty little bunny rabbits up the arse during predator/prey roleplay. They can't resist a sharp set of teeth and a big ol' knot, you see.

House prices are being kept artificially high because land barons and foreign investors (many of whom are laundering money) have captured an extremely corrupt government. If the government changes, there's still little that can be done because the UK economy is essential dependent on the property bubble and financial malpractice and the whole house of cards would tumble down if anyone tried to clean it up, something that definitely won't happen with the Tories at the helm.

There is precisely nothing that can be done about the housing crisis by regular people, either through democratic means or collective agency. The game is completely rigged against us. Even if we get the ball rolling now, the whole thing is going to come crashing down before we can possibly fix it. It will proceed with tedious inevitability until a combination of drastic changes will force a complete overhaul of the entire legal, economic and political order.

It is possible to escape on an individual level, if you're willing to up sticks and move (especially out of the country) or luck into money.

I think it's also worth considering from an economic perspective that there are lots of people with huge deposits that they still can't buy a house with, while the news is constantly focused on the "cost of living crisis". There are reports of starving people using their free bus pass to sit on a bus and ride around all day so they don't have to use their own heating at home, and meanwhile, thousands of people have 20-30 grand in the bank that they could spend whenever they want. So for a lot of us, there is no cost-of-living crisis at all; we can absorb any price increases whatsoever with our massive savings. But the national discourse focuses on homeowners who are poor instead. Renters who are rich should surely be laughing all the way to the bank; if you trust the news, we're the City bankers of the modern age. And we can't buy derelict ex-council houses because we can't afford them. It's enough to turn a man against the media.

Fewer people have those savings or are likely to be by able to build them with the current cost of living crisis, and those with savings are likely to soon lose them. House prices are now rising so fast that in the time it takes you to save for a deposit, the amount you need may rise faster than you can possibly save. Even if your savings accrue some interest, it doesn't matter because the interest rate on savings is going to be less than on any type of loan, including a new mortgage. It truly is a grim time to have aspirations of home ownership.

The worst thing is if you ever plan to save for anything else, the first thing you should do is get a mortgage, since your living costs will decrease thereafter. This is at a time when self-investment in training and certification is essential just to tread water in the job market. Grim grim grim.

>>9401 I'm not really one for 40-minute YouTube videos, but I watched three minutes of that and I wasn't impressed.

>That bloody doomsday clock again

It's bollocks. Everyone who says it's bollocks is right. It's a pointless gimmick made up by people with no more expertise than us on the actual end of the world, choosing to arbitrarily set a time based on their own subjective feelings.

>Build more goddamn houses

Nope. Some cities in America have tried just building more houses; they make the city much more desirable to live in so people move there and the house prices go up anyway. It doesn't solve the problem at all. And besides, we already have houses; people aren't sleeping in the streets due to the housing shortage. Most people have homes, but we don't own them; we rent them from someone else. Building more houses just builds more investment opportunities for the people who own the existing houses. It might help a bit, in the same way that banning people from wearing jeans would probably help with climate change a bit. There are better solutions to these problems.

>Some cities in America have tried just building more houses; they make the city much more desirable to live in so people move there and the house prices go up anyway.

If you're just going to do it in one or two places without any co-ordination then of course that will happen. But anyway there's a whole segment about the unique issues of America's housing market in the video you didn't watch.

>And besides, we already have houses; people aren't sleeping in the streets due to the housing shortage.

I think you'll find that was also addressed in the video you didn't watch.

>Building more houses just builds more investment opportunities for the people who own the existing houses.

Supply and demand mate. If there are loads to go around the prices are lower, the rent you can ask is lower, and the investment is nowhere near as lucrative. But this was addressed in the video you didn't watch.

>There are better solutions to these problems.

Go on then. I was asking.

If you're going to say rent controls or something like that, there's a substantial segment giving evidence why they don't work in the video you didn't watch.

Precisely. We're talking about a simple problem with a simple solution, but it has been intentionally over-complicated by people with a vested interest in the status quo.

People want affordable housing for their kids, but they also want to fund their retirement by ripping off someone else's kids. They don't want to admit that contradiction, so they pretend that housing doesn't obey the same economic laws as literally everything else in the world.

If we had a chronic shortage of shoes that was causing the price of shoes to increase much faster than inflation, we wouldn't be hemming and hawing over possible solutions, we'd just make more shoes. That problem only becomes complicated if half the population are shoe speculators or buy-to-let shoelords who actually want the price of shoes to keep rising forever.

>>9404 You can't really compare housing to shoes, though, because there isn't really a limit on how many shoes you can make. You could make a pair of shoes for everyone in the world, and everyone would have shoes. You could ask them in advance and they could even have the shoes they want. Meanwhile, if you want to buy the house that's opposite KFC so you can go to KFC every day, there is precisely one house opposite that KFC. You can't build everyone a house opposite KFC; the street would fill up and they'd have to demolish the wildly inferior Subway, and the primary school that doesn't serve breakfast at all. You can build houses elsewhere, but nobody will want them. It's like if there was a shortage of shoes but there could only be 50 pairs of shoes available in each size at any time. In that situation, the only answer would be to find the man with 15 pairs of size-8 Air Jordans and take the shoes from him.

If Britain had the same population density as Hong Kong, we'd have a population of 1.6 billion. This country feels crowded, but it's mostly empty. It would feel much less crowded if we built a few new towns with decent public transport.

Nobody actually chooses between a house directly opposite KFC or homelessness. They make trade-offs based on cost, location, size, quality and a variety of idiosyncratic factors. A handful of uninhabitable houses in very poor locations do have a market value of zero, but that's an edge case. The vast majority of houses are worth more than they would cost to build even if they're inconveniently located, poorly built, unattractive or cramped, because there simply aren't enough houses for people to have a real choice.

Increasing the supply of housing gives buyers and renters more choice, while reducing the bargaining power of sellers and landlords. You might not get your dream pair of Yeezys, but you'd probably prefer something from Off-White or Balenciaga over the tatty pair of Dunlop Green Flash you're currently spending half your income to rent.

>>9405 >the primary school that doesn't serve breakfast at all

Fake News: KFC doesn't do breakfast at all but many schools offer a breakfast programme for their students.

>>9408 I reckon I'm stuck in London until hybrid working sticks and they sort out the transport network. It's all well and good getting a house out in the sticks but it becomes unaffordable if I'm having to commute on a season ticket.