[ Return ] [ Entire Thread ] [ First 100 posts ] [ Last 50 posts ]

| >> | No. 7541

7541

One of the UK's most high profile stock-pickers has suspended trading in his largest fund as rising numbers of investors ask for their money back. Neil Woodford said after "an increased level of redemptions", investors would not be allowed to "redeem, purchase or transfer shares" in the fund. |

| >> | No. 7601

7601

I've been in on a meeting with members of Woodford's team. They've confirmed that:- |

| >> | No. 7602

7602

>>7601 |

| >> | No. 7604

7604

Financial Conduct Authority boss Andrew Bailey said fund rules may need amending in the wake of the Woodford fund suspension. In a letter penned for the Financial Times, Bailey said the suspension of the £3.7 billion fund last Monday had raised important questions about the UK’s regulatory approach towards investment in illiquid assets. |

| >> | No. 7606

7606

>>7602 |

| >> | No. 7608

7608

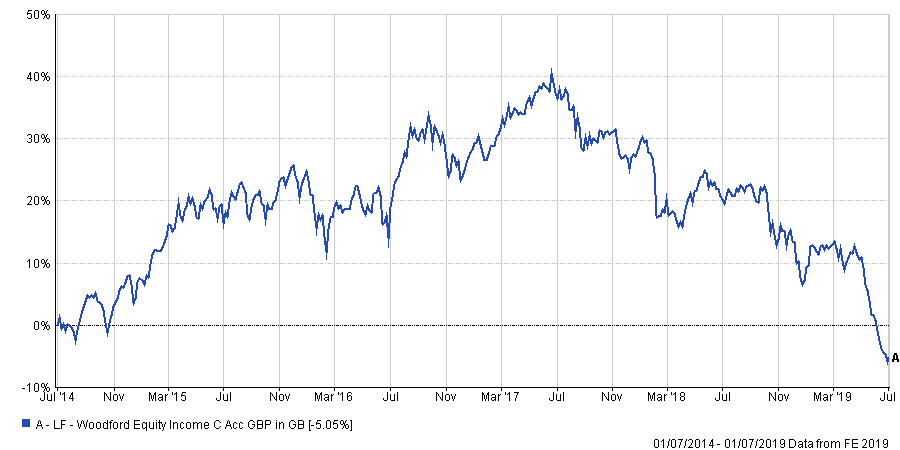

linechart.png  As expected... |

| >> | No. 7662

7662

It's now expected to open in December at the earliest. |

| >> | No. 7673

7673

>One of the UK's most high-profile stockpickers |

| >> | No. 7675

7675

linechart.png  >>7673 |

| >> | No. 7676

7676

>>7675 |

| >> | No. 7677

7677

>>7675 |

| >> | No. 7678

7678

>>7676 |

| >> | No. 7679

7679

>>7678 |

| >> | No. 7680

7680

>>7679 |

| >> | No. 7681

7681

>>7680 |

| >> | No. 7682

7682

>>7681 |

| >> | No. 7683

7683

>>7682 |

| >> | No. 7684

7684

>>7680 |

| >> | No. 7706

7706

Speaking of the cult of personality... |

| >> | No. 7709

7709

>>7706 |

| >> | No. 7710

7710

>>7709 |

| >> | No. 7711

7711

>>7706 |

| >> | No. 7712

7712

>>7709 |

| >> | No. 7713

7713

>>7712 |

| >> | No. 7717

7717

>>7710 |

| >> | No. 7718

7718

>>7717 |

| >> | No. 7797

7797

Neil Woodford’s stricken equity income fund to be shut down |

| >> | No. 7798

7798

He's thrown his toys out of the pram about being dismissed from his flagship fund by leaving the other two funds he ran. |

| >> | No. 7897

7897

Lads what do all your stocks and shares look like? |

| >> | No. 7898

7898

>>7897 |

| >> | No. 7899

7899

>>7898 |

| >> | No. 7900

7900

>>7897 |

| >> | No. 7901

7901

>>7899 |

| >> | No. 7902

7902

>>7901 |

| >> | No. 7903

7903

>>7901 |

| >> | No. 7904

7904

>>7900 |

| >> | No. 7905

7905

>>7902 |

| >> | No. 7906

7906

>>7905 |

| >> | No. 7908

7908

>>7897 |

| >> | No. 7909

7909

>>7906 |

| >> | No. 7930

7930

I'm looking at funds on the Vanguard website right now and there's a boggling array to choose from. How exactly do you go about picking the right one? I'm assuming if you've only got around 5k to invest then you're better off on the riskier side of the spectrum? |

| >> | No. 7932

7932

>>7930 |

| >> | No. 7933

7933

>>7930 |

| >> | No. 8476

8476

Neil Woodford: I’m back, like it or not |

| >> | No. 8477

8477

>>8476 |

| >> | No. 8478

8478

>>8477 |

| >> | No. 8479

8479

>>8477 |

| >> | No. 8480

8480

>>8478 |

| >> | No. 8481

8481

>>8480 |

| >> | No. 8482

8482

>>8481 |

| >> | No. 8559

8559

FCA first alerted to concerns over Neil Woodford’s business in 2015 |

[ Return ] [ Entire Thread ] [ First 100 posts ] [ Last 50 posts ]

|

Delete Post [] Password |