[ Return ] [ Entire Thread ] [ First 100 posts ] [ Last 50 posts ]

| >> | No. 3840

3840

The OFT have come out and said that many old (i.e. set up before 2001) pension schemes have high charges and offer savers poor value for money. They've also suggested a cap for auto-enrolment schemes, but it's going to be an almost meaningless gesture as you'd be very hard pressed to find a provider offering auto-enrolment terms with annual management charges greater than 1% anyway. |

| >> | No. 9046

9046

|

| >> | No. 9047

9047

>>9045 |

| >> | No. 9083

9083

I've got about £45k in a couple of old workplace pension schemes. How do I figure out the best place to move them? |

| >> | No. 9084

9084

>>9083 |

| >> | No. 9085

9085

>>9084 |

| >> | No. 9105

9105

>>9085 |

| >> | No. 9192

9192

As a basic rate taxpayer is there any point in me paying more into a pension than any employer matching? Salary sacrifice isn't an option. |

| >> | No. 9225

9225

>>9083 here again. |

| >> | No. 9227

9227

>>9225 |

| >> | No. 9228

9228

linechart (1).png

>>9227 |

| >> | No. 9257

9257

Fuck it. I've set up an account with AJ Bell and requested the transfer of my Aviva pensions with them. I just need to hope things go down rather than up over the next 2-4 weeks whilst I'm out of the market. |

| >> | No. 9258

9258

>>9257 |

| >> | No. 9259

9259

>>9258 |

| >> | No. 9260

9260

>>9259 |

| >> | No. 9520

9520

>Spiralling inflation, volatile financial markets and the soaring cost of living are leading to the “great unretirement”, with research suggesting retired people are returning to the workplace. |

| >> | No. 9634

9634

So me and the wife collectively earn just over £100k. Before you think we're rolling in it, we live in the capital so the money doesn't go as far and the mortgage is crippling us. That said, with a nipper on the way, apparently we get less help because of our collective earnings, in terms of child benefit and the prospective 30 hours free childcare. |

| >> | No. 9635

9635

>>9634 |

| >> | No. 9636

9636

>>9634 |

| >> | No. 9643

9643

Anyone else slightly concerned by the pensions announcement in the Budget? They're scrapping the lifetime allowance but are freezing the amount of tax free cash you can take to £268,275, which was 25% of the allowance. It feels like this is a slippery slope and in a few years they'll start revising this downwards until they decide you can only take out £20,000 out tax free or something. |

| >> | No. 9653

9653

Capture1.png

Decided to let the Muzzies run my pension. You know what they say: past performance is a guarantee of future performance. |

| >> | No. 9654

9654

>>9653 |

| >> | No. 9655

9655

>>9654 |

| >> | No. 9656

9656

>>9655 |

| >> | No. 9657

9657

>>9656 |

| >> | No. 9658

9658

>>9657 |

| >> | No. 9781

9781

Would it make sense to pay off as little as possible on a mortgage and instead overpay into a pension to use a tax-free lump sum at 55/57 to clear the mortgage then? |

| >> | No. 9782

9782

>>9781 |

| >> | No. 9783

9783

>>9782 |

| >> | No. 9784

9784

>>9781 |

| >> | No. 9785

9785

>>9784 |

| >> | No. 9786

9786

Another point I forgot to make, endowment funds would have to pay tax internally deemed equivalent to basic rate tax that you wouldn't have with a pension (or ISAs and GIAs) so if a pension fund returned 5% then the same fund in an endowment would return 4%. |

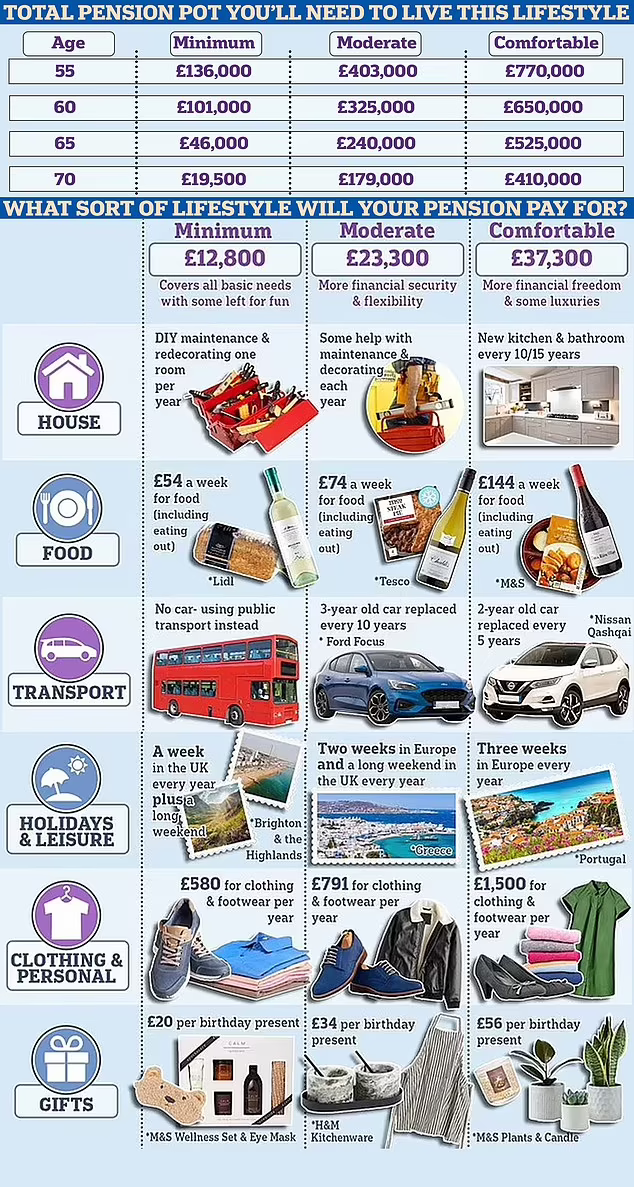

| >> | No. 9795

9795

79747553-12933185-image-a-5_1704718719295.png

Looks like Lidl's on the menu, lads. |

| >> | No. 9796

9796

>>9795 |

| >> | No. 9797

9797

Transferred my SIPP to Interactive Investor for their cashback offer, but it looks like the S&P500 going up while I was out the market for two weeks has more than wiped that out. |

| >> | No. 9870

9870

I have some money in a Standard Life pension. I'm not building it and there's not enough in there to justify its existence - is there any way I can withdraw the capital? |

| >> | No. 9871

9871

>>9870 |

| >> | No. 9872

9872

When you get sacked, do you still pay pension contributions on your final pay? |

| >> | No. 9876

9876

There's a lot of bright ideas floating around at the minute. |

| >> | No. 9877

9877

>>9876 |

| >> | No. 9917

9917

I just had a look at my pension. In 2055, I will have an annual income of around £17,000 a year, including the state pension. My rewards from my career will be about £5000 a year. Obviously I'll be able to live cheaply once I've paid off my mortgage, but fucking hell. Pensions are such a bloody scam. Considering what inflation will do to an income of 17 grand a year in a little over 30 years, I don't see why I'm bothering. |

| >> | No. 9918

9918

>>9917 |

| >> | No. 10121

10121

>Denmark is set to have the highest retirement age in Europe after its parliament adopted a law raising it to 70 by 2040. Since 2006, Denmark has tied the official retirement age to life expectancy and has revised it every five years. It is currently 67 but will rise to 68 in 2030 and to 69 in 2035. The retirement age at 70 will apply to all people born after 31 December 1970. |

| >> | No. 10122

10122

>>10121 |

| >> | No. 10123

10123

>>10121 |

| >> | No. 10145

10145

>People retiring in 2050 will be worse off than pensioners today, the government has warned, unless action is taken to boost retirement savings. |

| >> | No. 10146

10146

>>10145 |

| >> | No. 10147

10147

>>10146 |

| >> | No. 10148

10148

>>10146 |

| >> | No. 10149

10149

>>10148 |

| >> | No. 10150

10150

>>10149 |

[ Return ] [ Entire Thread ] [ First 100 posts ] [ Last 50 posts ]

|

Delete Post [] Password |