There are some weird responses early on in this thread, but anyway:

I think it is possible, but I think it's made easier perhaps in the US where comparative salaries tend to be higher.

In the UK we are compensated for that fact with a strong safety net and other benefits (guaranteed paid leave for a start), so our wages are lower making it slightly harder.

I still think it's possible though and it makes a lot of sense, it's just about discipline and a bit of luck really.

Guess I did it to some extent. Bit of luck + successful tech IPO + not pissing it all away like most people do and I left my career last year with no intention of going back into full time employment if I can help it. Early thirties.

While I don't think pursuing FI/RE is for everyone, it's definitely worth reading a few of the popular blogs purely for a different perspective on money, budgeting, investing etc. r/fireuk might be of interest.

It's difficult to make the numbers stack up. Most people are barely saving enough to retire at 67.

The most prudent way of funding retirement is through an annuity, which is like the opposite of life insurance - you pay a lump sum up front and get a guaranteed annual payment for life. A sensible annuity includes an escalator, meaning that the payment amount is increased annually to offset the effects of inflation.

If you want to retire at 55, you'll need to pay ~£38,500 to get an annuity paying £1,000 a year with a 3% escalator. If you want a retirement income of £16,000, you'll need a pension pot of £616,000. To accrue that amount, you'll need to consistently save at least £550 a month for 35 years. Not many people are able or willing to put away that amount of money. You'll probably have to save a lot more than that, because annuity rates are tied to life expectancy. They have more than halved over the past 20 years and that trend seems to be continuing.

The numbers get exponentially worse if a) you're starting late or b) you want to retire even earlier. If you're 35 and you want to retire at 55, you'll need to save at least £1,400 a month to have a comfortable income.

A lot of people who aspire to retire early are pinning their hopes on various "passive income" schemes, but that's a very risky strategy. It's perfectly possible to make a couple of grand a month through affiliate marketing, self-publishing or all manner of other relatively low-effort business ventures. If you're smart, confident and resourceful, it's not necessarily very difficult. The problem is that those income streams are really rather fickle. You might have two dozen books selling well on the Kindle store, but those sales will inevitably dwindle over time unless you're continually putting out new content. You might have a few blogs bringing in a few hundred quid a month each through advertising or affiliate links, but a change in Google's algorithm could kill your traffic overnight. If your business goes to shit when you're young and healthy, it's a massive pain in the arse. You might have to work like a dog to turn things around, do a bit of Uber driving to keep the wolf from the door or go back to working full-time. If your income collapses when you're elderly, then you're up shit creek.

I strongly encourage people to give serious thought to their retirement options and start planning early, but I wouldn't get carried away with ideas about retiring to a Caribbean island at the age of 40.

>>12207 > The most prudent way of funding retirement is through an annuity

Not for early retirement, no.

> A lot of people who aspire to retire early are pinning their hopes on various "passive income" schemes

The common approach for FI/RE is investing at least 25x annual expenses in low cost global equity trackers and relying on (average) 7% long term global stock growth minus 3% (average) inflation to withdraw and live off 4% a year indefinitely. Those percentages are debatable, but most people seriously pursing FI do so with stock market investments.

Drawing down from investments carries substantial risk. Over the past 30 years, we've had two recessions that led to a >40% drop in the FTSE all-share. Global diversification helps a bit, but it can't mitigate against massive international shocks. If one of those recessions hits during the early years of your retirement, it can completely derail your plans. You're in double trouble - the value of your portfolio has collapsed and you need to eat into your much-diminished capital to pay your bills. There's a very real possibility that the era of 7% growth is over forever. In the UK, drawing down carries substantial tax implications.

We're still talking about a much larger pension pot than most working people could reasonably expect to build. The average 55 year old only has a pension pot of ~£105,000.

Well that's entirely possible, yeah. I've done that with a decent paying job and sensible investments. I'm barely 30 but if I chose to I think I could retire now. I'd not live a particularly glamorous life but I could do it.

>>12209 This. I didn't see a single mention on the website of sequence risk when it comes to drawing an income.

If the target you aim for is 25x your annual expenditure then this largely seems to be a pipe dream unless you're on a very high salary. It's good to get into the habit of investing, but that's literally it.

The article is also geared more towards Americans and the difference tax status they'll have for the investment wrappers over there; a pension is generally your best bet here due to tax relief and employer contributions. Index trackers are much cheaper over there and actively managed funds, at least the top ones, tend to perform better over here.

I'm prepared to be a thick cunt but I've been told that £2million is that magic number where you can live off your interest providing you invested well enough and you put down a deposit before coasting.

FIRE doesn't appeal to me but I do try to live frugally. I would try and FIRE but I think I'm missing out on an exceptionally lucrative career and the dedication plus a partner who you can pay off a house with easily.

Having said that reading the reddit forums on it is surprisingly interesting and in some way inspiring.

I think financial security is seriously underrated too, it's really calming knowing that you can lose your job and still have coins in the bank to survive, or if you absolutely must go live on a beach somewhere for a while.

Speaking of which, I kind of like living a simple, frugal kind of life. I don't eat plain rice for tea, but I do watch my money and avoid excessive luxuries. Without wanting to sound holier than thou but undoubtedly doing so - I moved home recently as my job sent me somewhere commutable from where my parents live so I decided to save some money (early-mid twenties life and all that). A lovely neighbour asked my mum if something had gone terribly wrong because I was wearing my own clothes and no longer wearing suits every day and I am still driving around an old banger.

I'm getting paid more than ever in a really good job for which I'm eternally grateful, but I guess to the neighbours they see me wearing casual clothes and driving my old car, so it probably looks like I'm having a bad time.

It makes me wonder how many people you pass on the street who are wadded but you'd never look twice, and how many are driving massive Audis without two pennies to rub together.

This is very good, thanks. That's one of the ingredients missing from my own spreadsheet; I've worked out my expenditure for every month but have no savings.

I can see you've got a couple of things going with Abundance, something I intended to out money into in the future. In fact a few 'ethical investment' threads were started by me a while back.

Truthfully I've only just recently got my first full-time job, and it's still £20k per year. I don't really know where to start. I suppose an ISA would be a pretty sensible first point to dump money.

I only vaguely browsed the thread because you all seem to be chatting breeze. I have a 50% share in a tech company currently valued at $330 million. If I don't walk off with $50 million after taxes or we never get squired then my retirement plan is a drugs overdose which given what I just posted in /101/ I might need to take a loan out for, ho ho.

In the states the majid number you hear bandied about is $1 million to get a decent wage. That's because the S&P outperforms the FTSE at about 5-3 and because cost of living in America (especially in the sticks is cheaper than a council house and and Iceland meals here in the UK.

I've done my research and I think the magic number here in £2million in the bank. Properly applied you can take £40k a month out pay income tax on that (providing you didn't pay income tax when you earned otherwise only pay on the interest bla bla) and live a fairly modest life off that ,,,, Fuck you money is somewhere about £30 mill in the bank.

If any of you cunts want my advice, and you don't, learn a bit about the blockchain, make an alt coin that isn't derived from eth, maybe try to be monero but without the high transaction costs. Give away say £1000 in an airdrop and have a pre-sale at 50% up to £20,000.

Then steal all the money and put it in a swiss account.

You'd probabaly make 5-6 figures if you can make a half decent website and are provably not chinese, indian, or easter european (who are doing al the scam coins these days).

Either that or invest 6 years of your life into developing a massive multi-substance abuse drugs habbit that has you waiting for the chemist to open so you can buy your Ambien whiole you're worth $1,650,000.00 on paper but are owed 20 grand in back pay and your wife left but and your retirement plan is suicide by cop.

Anyway.

Yeah it's possible to retire early but you need either capital to derive income from or assets to leverage (e.g. property).

Don't fall for pyramid scams or get rich quick schemes you mong. I've been working for 14 years now and all I have is 170k in the bank and an imaginary $1,650,000.

The valuation of my company? No $300 million USD, 50% stake. When we're acquired I assume I'll have to pay all kinds of taxes in both the UK and the US and maybe even the country I live (which I'll leave before any. Anway 150 million taxed 30% by the US and 50% by the UK should laeave me around $50 with after layers free so I can finally fetire to shoot smack into the vein under my cock and actually get down to running my free, non-profit niche courthouse porn company that I'v alays wanted to run.

You know, things like a middle class Sixth Form (18+ obviously) girl called Charlottle who's worked hard for weeks so she shove a bag of six Aldi value apples up her her arse one my one.

Or a Goldsmith's student called Chloe who let you tie her up with the gold ire her daddy Tarquin bought Special for her new installation and then go to work on her tits andf fanny with her staple gun.

Or maybe Imogen who works with horses and is basically a kept daughter from an Oxbridge family. Basically her scenes would be crying about how her parents sent he to boarding school while a Vicky Pollard look-a-like turns her arsehole into an inside-out pink sock with an actual horse cock vibrator.

I'm not saying that everything is possible, that that £30 million opens a lot of doors if you wan to run a non-for-profit porn company.

So you're saying you're going to actually lop a penis off a horse, get a taxidermist to preserve it and then insert the necessary gadgetry to make it vibrate - possibly with a base unit attached so you can make said appendage wiggle?

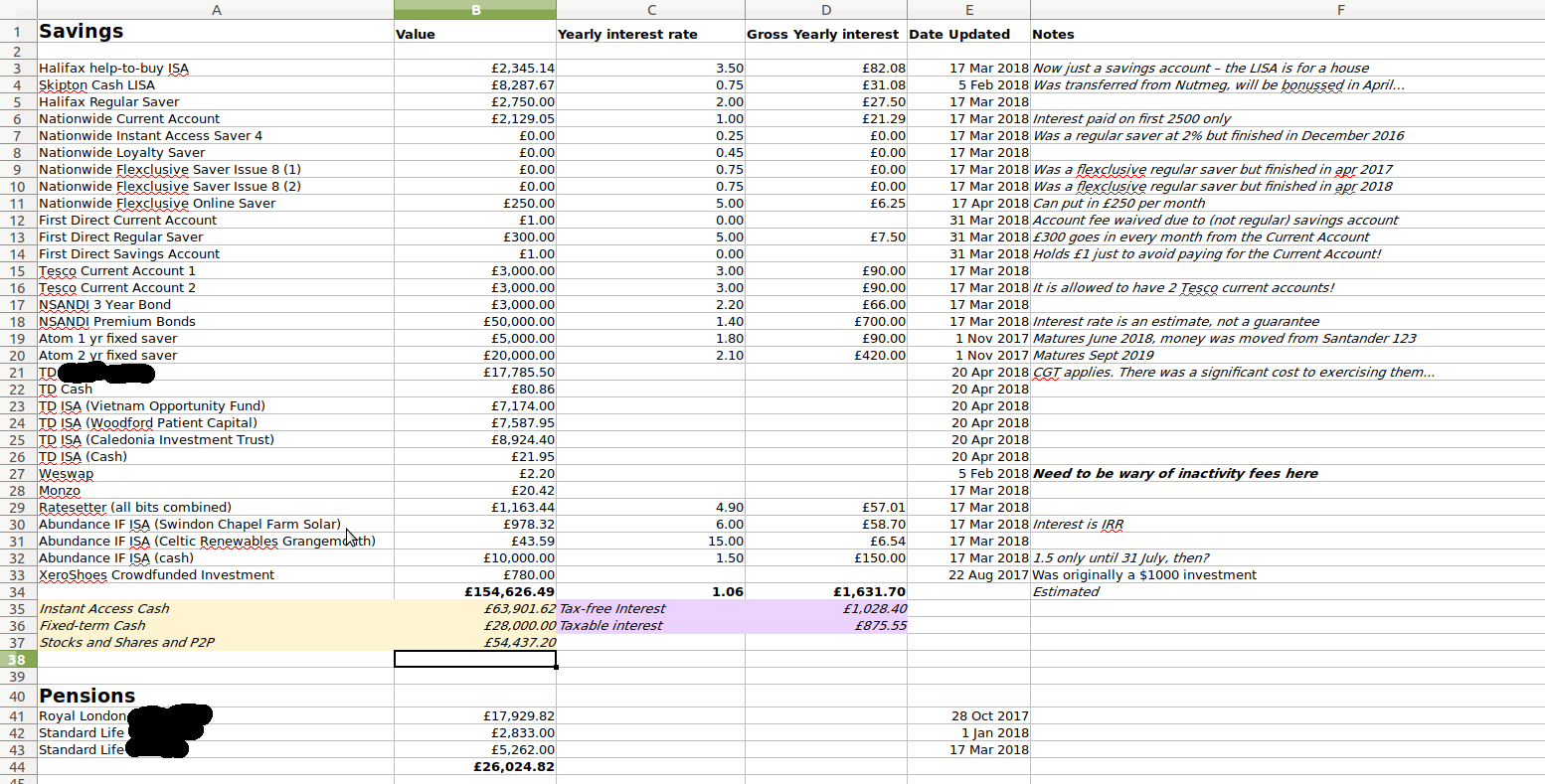

Savingslad, the more I look at your spreadsheet the more impressed I am by your choices. I've heard of Abundance before, but was searching for something like TD for years without success. Did you find all these accounts by trial and error? Do you have an advisor? How can I learn?

Also, what are the limitations on the help-to-buy ISA? I could happily dump £1200 into a help-to-buy right now, but I need all the savings available for possibly going away to study in September. Can I just claim the top-up then withdraw a few months later?

>>12282 There are limits to how much you can pay in, depending on the provider.

My halifax ISA had an opening limit of £1000. After that, you can only pay in by standing order, and a max of £200 per month.

You can withdraw whenever you want, but there's absolutely no point because you're not paid interest on any balance that has been taken out that year.

The top-up is only paid if you take out a mortgage. There's absolutely no other way to get it. Same with the lifetime ISA.

It is impressive, I have roughly the same amount in cash savings as him (but nothing even approaching a pension scheme) but it's all sat earning 0.5% interest in one account. I really need to get my act together and start applying that money in more profitable ways.

I should probably be doing something relatively more profitable than just an ISA (not that I have a UK tax liability) but I'm fully aware of how utterly futile having that much cash sitting in 0.5% savings accounts is, so no need to screw me out over it.

I just need to figure out what the fuck to actually do with it, other than stick it in a 20 year fixed rate bond for my kid as a form of post-uni trust fund or something. I mean it's either that or blow it on drugs.

I wasn't intending to screw you out, just saying there's certainly some steps you could take even today to improve your position.

When I started making nice money (christ is .gs really this full of fiscally endowed young gentlemen?) I just went straight to a financial planner, as I'm well aware I'd have pissed it all away otherwise. If I had been left to my own devices I'd likely have done what you're doing, either sat in a high street savings account really designed for a few grand at most, or 'invested' into the columbian powder trade. I was quite happy to defer to professionals.

>>12287 >>12283 here, actually I'm not loaded spreadsheet lad, I'm some other guy.

Myself, I'm 28 and have £6K in an ISA and about 2 months pay in my current account before payday.

>>12290 Right if you've got £170,000 the first step is to have three to six month's expenditure in cash as an emergency fund. That means you've probably got at least £160,000 to play with.

The next step is largely dependent on what your aims and objectives are, including when you're planning to make use of this money, and how much you can afford to lose.

What are you aiming for? To own a home, go on lots of nice holidays, to reduce your hours at work, to retire early, etc.

> I wasn't intending to screw you out, just saying there's certainly some steps you could take even today to improve your position.

Sorry lad, to intent to offend. But I've had people shout at me before for not putting it in pensions / this / that the other. I know I'm grossly misapplying the money I just never seem to get around to actually finding a financial advisor I feel like I can trust (I'm half bright enough to know that my Santander Select personal manager gimboid just wants to earn commission selling me financial products.

That basically leaves me gimping around trying to find someone who will accept money to give me professional and impartial advice, and that seems like a lot of work (or time to find, rather) to a chap who is going to take his first recreational break from work since last Sunday night in about forty-five minutes.

>>12295 > the first step is to have three to six month's expenditure in cash as an emergency fund

The 20k in the separate account is my six month survival fund. When clients don't pay on time, lose invoices, or banks fuck up I have money to live on until things get unfucked again and suddenly people start paying three invoices at once and so on.

> What are you aiming for? To own a home, go on lots of nice holidays, to reduce your hours at work, to retire early, etc.

My aim is to work myself to death until my company either gets acquired or goes bankrupt or I and my business partner sign a stress-induced murder-suicide pact and shoot each other in the head with illegally modified spud guns, or something.

I don't really have a backup plan. If this whole business thing falls through I'll probably take a six month sabbatical and then be forced back into the real world of commutes, offices, regular salaries, and God Above Forbid having to wear a fucking suit again.

If / when that happens I'll invest the leftover 150 or so in some kind of life insurance thingamajig / trust fund thingamajig so the sprog has some decent money to deal with university and the post-graduation doldrums (I have about as much faith in private pension funds as I do in me ever reaching the state retirement age which will probably be about 80 by the time I get there).

So, no plans really, other than "get acquired or die trying".

I just wish I was getting 5% interest on my 150k, not 0.5% You get 5%, why don't I get 5%? Why isn't my bank manager getting me 5%? Bastard must have died.

• Do you have key person cover if anything happens to your business partner?

• Do you have income protection if you're unable to work due to sickness or injury?

• Do you have any form of life cover to either pay off a mortgage, cover any other debts or to provide your missus or sprog with a lump sum/regular income in the event of your death?

The advantage of running your own business is that you should be able to arrange the company to pay for these so this would be more tax efficient than paying out of your own pocket.

When we get to pensions it'd most likely be better out of your own pocket than the company if you're a higher rate taxpayer because the rate of company tax relief would be much lower than higher rate income tax relief, particularly if it means you can reclaim either your personal allowance or the child benefit tax charge.

It's often easier to be reasonably good at two mutually beneficial things - a web developer with some training in marketing, an accountant who really understands the specifics of the construction industry, an electrician who knows about AV installation or home automation.

All I can say is that personally I just figured out a way to become uniquely useful then charged accordingly. That may sound broad but anyone in any industry can do a version of that. The latter point is important, I have worked with people far more clever than me who just lacked the sense (or perhaps the drive) to realise they were far more useful than their salary made out.

I always assumed that the key to retiring early was owning multiple properties outright and living off the rental income, but I've never properly researched it so could be way off the mark.

>>12304 It's always been taxable income. The ongoing change removes the mortgage interest deductible which, yes, will increase taxable income for many.